A Fresh Look at How to Measure SaaS Churn Rates

[Editor's note: revised 3/27/17 with changes to some definitions.]

It’s been nearly three years since my original post on calculating SaaS renewal rates and I’ve learned a lot and seen a lot of new situations since then. In this post, I’ll provide a from-scratch overhaul on how to calculate churn in an enterprise SaaS company [1].

While we are going to need to “get dirty” in the detail here, I continue to believe that too many people are too macro and too sloppy in calculating these metrics. The details matter because these rates compound over time, so the difference between a 10% and 20% churn rate turns into a 100% difference in cohort value after 7 years [2]. Don't be too busy to figure out how to calculate them properly.

The Leaky Bucket Full of ARR

I conceptualize SaaS companies as leaky buckets full of annual recurring revenue (ARR). Every time period, the sales organization pours more ARR into the bucket and the customer success (CS) organization tries to prevent water from leaking out [3].

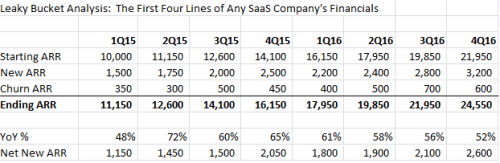

This drives the leaky bucket equation, which I believe should always be the first four lines of any SaaS company’s financial statements:

Starting ARR + new ARR – churn ARR = ending ARR

Here’s an example, where I start with those four lines, and added two extra (one to show a year over year growth rate and another to show “net new ARR” which offsets new vs. churn ARR):

For more on how to present summary SaaS startup financials, go here.

Half-Full or Half-Empty: Renewals or Churn?

Since the renewal rate is simply one minus the churn rate, the question is which we should calculate? In the past, I favored splitting the difference [4], whereas I now believe it’s simpler just to talk about churn. While this may be the half-empty perspective, it’s more consistent with what most people talk about and is more directly applicable, because a common use of a churn rate is as a discount rate in a net present value (NPV) formula.

Thus, I now define the world in terms of churn and churn rates, as opposed to renewals and renewal rates.

Terminology: Shrinkage and Expansion

For simplicity, I define the following two terms:

- Shrinkage = anything that makes ARR decrease. For example, if the customer dropped seats or was given a discount in return for signing a multi-year renewal [5].

- Expansion = anything that makes ARR increase, such as price increases, seat additions, upselling from a bronze to a gold edition, or cross-selling new products.

Key Questions to Consider

The good news is that any churn rate calculation is going to be some numerator over some denominator. We can then start thinking about each in more detail.

Here are the key questions to consider for the numerator:

- What should we count? Number of accounts, annual recurring revenue (ARR), or something else like renewal bookings?

- If we’re counting ARR should we think at the product-level or account-level?

- To what extent should we offset shrinkage with expansion in calculating churn ARR? [6]

- When should we count what? What about early and late renewals? What about along-the-way expansion? What about churn notices or non-payment?

Here are the key questions to consider for the denominator:

- Should we use the entire ARR pool, that portion of the ARR pool that is available to renew (ATR) in any given time period, or something else?

- If using the ATR pool, for any given renewing contract, should we use its original value or its current value (e.g., if there has been upsell along the way)?

What Should We Count? Logos and ARR

I believe the two metrics we should count in churn rates are

- Logos (i.e., number of customers). This provides a gross indication of customer satisfaction [7] unweighted by ARR, so you can answer the question: what percent of our customer base is turning over?

- ARR. This provides a very important indication on the value of our SaaS annuity. What is happening to our ARR pool?

I would stay completely away from any SaaS metrics based on bookings (e.g., a bookings CAC, TCV, or bookings-based renewals rate). These run counter to the point of SaaS unit economics.

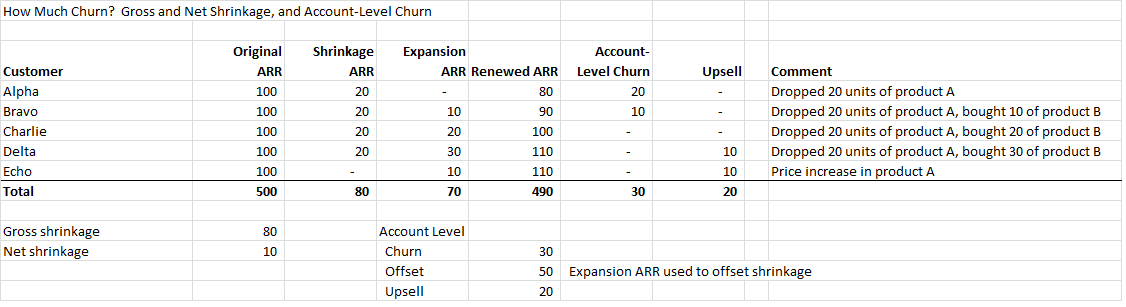

Gross and Net Shrinkage; Account-Level Churn

Let’s look at a quick example to demonstrate how I now define gross and net shrinkage as well as account-level churn [8].

Gross shrinkage is the sum of all the shrinkage. In the example, 80 units.

Net shrinkage is the sum of the shrinkage minus the sum of the expansion. In the example, 80-70 = 10 units.

To calculate account-level churn, we proceed, account by account, and look at the change in contract value, separating upsell from the churn. The idea is that while it’s OK to offset shrinkage with expansion within an account that we should not do so across accounts when working at the account level [9]. This has the effect of splitting expansion into offset (used to offset shrinkage within an account) and upsell (leftover expansion after all account-level shrinkage has been offset). In the example, account-level churn is 30 units.

Make the important note here that how we calculate you churn – and specifically how we use expansion ARR to offset shrinkage—not only affects our churn rates, but our reported upsell rates as well. Should we proudly claim 70 units of upsell (and less proudly 80 units of churn), 30 units of churn and 20 of upsell, or simply 10 units of churn? I vote for the second.

While working at the account-level may seem odd, it is how most SaaS companies work operationally. First, because they charter customer success managers (CSMs) to think at the account level, working account by account doing everything they can to preserve and/or increase the value of the account. Second, because most systems work at and finance people think at the account level – e.g., “we had a customer worth 100 units last year, and they are worth 110 units this year so that means upsell of 10 units. I don’t care how much is price increase vs. swapping some of product A for product B.” [11]

So, when a SaaS company reports “churn ARR,” in its leaky bucket analysis, I believe they should report neither gross churn nor net churn, but account-level churn ARR.

Timing Issues and the Available to Renew (ATR) Concept

Churn calculations bring some interesting challenges such as early/late renewals, churn notices, non-payment, and along-the-way expansion.

A renewals booking should always be taken in the period in which it is received. If a contract expires on 6/30 and the renewal is received in on 6/15 it should show up in 2Q and if received on 7/15 it should up in 3Q.

For churn rate calculations, however, the customer success team needs to forecast what is going to happen for a late renewal. For example, if we have a board meeting on 7/12 and a $150K ARR renewal due 6/30 has not yet been happened, we need to proceed based on what the customer has said. If the customer is actively using the software, the CFO has promised a renewal but is tied up on a European vacation, I would mark the numbers “preliminary” and count the contract as renewed. If, however, the customer has not used the software in months and will not return our phone calls, I would count the contract as churned.

Suppose we receive a churn notice on 5/1 for a contract that renews on 6/30. When should we count the churn? A Bessemer SaaS fanatic would point to their definition of committed monthly recurring revenue (CMRR) [12] and say we should remove the contact from the MRR base on 5/1. While I agree with Bessemer’s views in general -- and specifically on things like on preferring ARR/MRR to ACV and TCV -- I get off the bus on the whole notion of “committed” ARR/MRR and the ensuing need to remove the contract on 5/1. Why?

- In point of fact the customer has licensed and paid for the service through 6/30.

- The company will recognize revenue through 6/30 and it’s much easier to do so correctly when the ARR is still in the ARR base.

- Operationally, it’s defeatist. I don’t want our company to give up and say “it’s over, take them out of the ARR base.” I want our reaction to be, “so they think they don’t want to renew – we’ve got 60 days to change their mind and keep them in.” [13]

We should use the churn notice (and, for that matter, every other communication with the customer) as a way of improving our quarterly churn forecast, but we should not count churn until the contract period has ended, the customer has not renewed, and the customer has maintained their intent not to renew in coming weeks.

Non-payment, while hopefully infrequent, is another tricky issue. What do we do if a customer gives us a renewal order on 6/30, payable in 30 days, but hasn’t paid after 120? While the idealist in me wants to match the churn ARR to the period in which the contract was available to renew, I would probably just show it as churn in the period in which we gave up hope on the receivable.

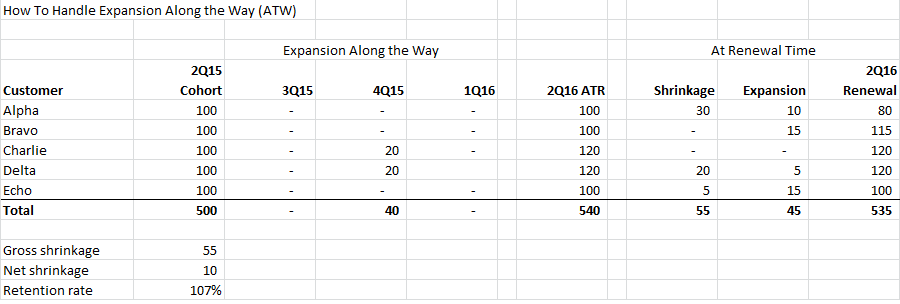

Expansion Along the Way (ATW)

Non-payment starts to introduce the idea of timing mismatches between ARR-changing events and renewals cohorts. Let’s consider a hopefully more frequent case: ARR expansion along the way (ATW). Consider this example.

To decide how to handle this, let’s think operationally, both about how our finance team works and, more importantly, about how we want our customer success managers (CSMs) to think. Remember we want CSMs to each own a set of customers, we want them to not only protect the ARR of each customer but to expand it over time. If we credit along-the-way upsell in our rate calculations at renewal time, we shooting ourselves in the foot. Look at customer Charlie. He started out with 100 units and bought 20 more in 4Q15, so as we approach renewal time, Charlie actually has 120 units available to renew (ATR), not 100 [14]. We want our CSMs basing their success on the 120, not the 100. So the simple rule is to base everything not on the original cohort but on the available to renew (ATR) entering the period.

This begs two questions:

- When do we count the along-the-way upsell bookings?

- How can we reflect those 40 units in some sort of rate?

The answer to the first question is, as your finance team will invariably conclude, to count them as they happen (e.g., in 4Q15 in the above example).

The answer to the second question is to use a retention rate, not a churn rate. Retention rates are cohort-based, so to calculate the net retention rate for the 2Q15 cohort, we divide its present value of 535 by its original value of 500 and get 107%.

Never, ever calculate a retention rate in reverse – i.e., starting a group of current customers and looking backwards at their ARR one year ago. You will produce a survivor biased answer which, stunningly, I have seen some public companies publish. Always run cohort analyses forwards to eliminate survivor bias.

Off-Cycle Activity

Finally, we need to consider how to address off-cycle (or extra-cohort) activity in calculating churn and related rates. Let’s do this by using a big picture example that includes everything we’ve discussed thus far, plus off-cycle activity from two customers who are not in the 2Q16 ATR cohort: (1) Foxtrot, who purchased in 3Q14, renewed in 3Q15, and who has not paid, and (2) George, who purchased in 3Q15, who is not yet up for renewal, but who purchased 50 units of upsell in 2Q16.

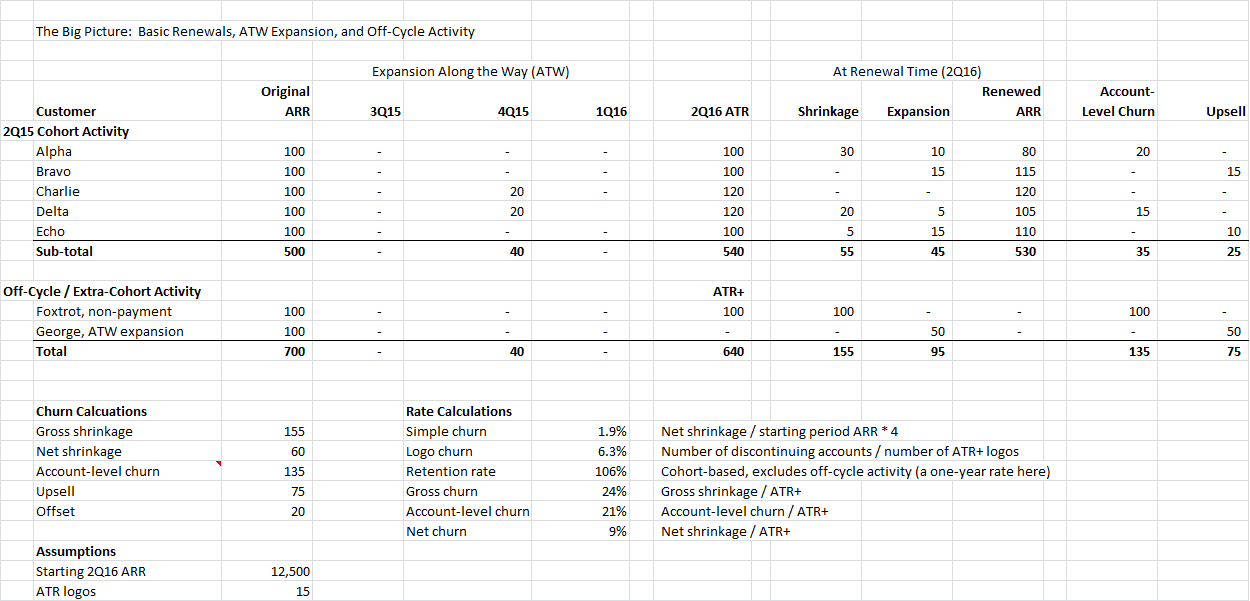

Foxtrot should count as churn in 2Q16, the period in which we either lost hope of collection (or our collections policy dictated that collection we needed to de-book the deal). [15]

George should count as expansion in 2Q16, the period in which the expansion booking was taken.

The trick is that neither Foxtrot nor George is on a 2Q renewal cycle, so neither is included in the 2Q16 ATR cohort. I believe the correct way to handle this is:

- Both should be factored into gross, net, account-level churn, and upsell.

- For rates where we include them in the numerator, for consistency’s sake we must also include them in the denominator. That means putting the shrinkage in the numerator and adding the ATR of a shrinking (or lost) account in denominator of a rate calculation. I’ll call this the “+” concept, and define ATR+ as inclusive of such additional logos or ARR resulting from off-cycle accounts [16].

Rate Calculations

We are now in the position to define and calculate the churn rates that I use and track:

- Simple churn rate = net shrinkage / starting period ARR * 4. Or, in English, the net change in ARR from existing customers divided by starting period ARR (multiplied by 4 to annualize the rate which is measured against the entire ARR base). As the name implies, this is the simplest churn rate to calculate. This rate will be negative whenever expansion is greater than shrinkage. Starting period ARR includes both ATR and non-ATR contracts (including potentially multi-year contracts) so this rate takes into account the positive effects of the non-cancellability of multi-year deals. Because it takes literally everything into account, I think this is the best rate for valuing the annuity of your ARR base.

- Logo churn rate = number of discontinuing logos / number of ATR+ logos. This rate tells us the percent of customers who, given the chance, chose to discontinue doing business with us. As such, it provides an ARR-unweighted churn rate, providing the best sense of “how happy” our customers are, knowing that there is a somewhat loose correlation between happiness and renewal [16]. Remember that ATR+ means to include any discontinuing off-cycle logos, so the calculation is 1/16 = 6.3% in our example.

- Retention rate = current ARR [time cohort] / time-ago ARR [time cohort]. In English, the current ARR from some time-based cohort (e.g., 2Q15) divided by the year-ago ARR from that same cohort. Typically we do this for the one-year-ago or two-years-ago cohorts, but many companies track each quarter’s new customers as a cohort which they measure over time. Like simple churn, this is a great macro metric that values the ARR annuity, all in.

- Gross churn rate = gross shrinkage / ATR+. This churn rate is important because it reveals the difference between companies that have high shrinkage offset by high expansion and companies which simply have low shrinkage. Gross churn is a great metric because it simply shows the glass half-empty view: at what rate is ARR leaking out of your bucket before offset it with refills in the form of expansion ARR.

- Account-level churn rate = account-level churn / ATR+. This churn rate foots to the reported churn ARR in our leaky bucket analysis (which uses account-level churn), partially offsets shrinkage with expansion at an account-level, and is how most SaaS companies actually calculate churn. While perhaps counter-intuitive, it reflects a philosophy of examining, at an account basis, what happens to value of our each of our customers when we allow shrinkage to be offset by expansion (which is what we want our CSM reps doing) leaving any excess as upsell. This should be our primary churn metric.

- Net churn rate = net shrinkage / ATR+. This churn rate offsets shrinkage with expansion not at the account level, but overall. This is similar to the simple churn rate but with the disadvantage of looking only at ATR and not factoring in the positive effects of non-cancellability of multi-year deals. Ergo, I prefer using the simple churn rate to the net churn rate in valuing the SaaS annuity.

# # #

Notes

[1] Replacing these posts in the process.

[2] The 10% churn group decays from 100 units to 53 in value after 7 years, while the 20% group decays to 26.

[3] We’ll sidestep the question of who is responsible for installed-based expansion in this post because companies answer it differently (e.g., sales, customer success, account management) and the good news is we don’t need to know who gets credited for expansion to calculate churn rates.

[4] Discussing churn in dollars and renewals in rates.

[5] For example, if a customer signed a one-year contract for 100 units and then was offered a 5% discount to sign a three-year renewal, you would generate 5 units of ARR churn.

[6] Or, as I said in a prior post, should I net first or sum first?

[7] And yes, sometimes unhappy customers do renew (e.g., if they’ve been too busy to replace you) and happy customers don’t (e.g., if they get a new key executive with different preferences) but counting logos still gives you a nice overall indication.

[8] Note that I have capitulated to the norm of saying “gross” churn means before offset and thus “net” churn means after netting out shrinkage and expansion. (Beware confusion as this is the opposite of my prior position where I defined “net” to mean “net of expansion,” i.e., what I’d now call “gross.”)

[9] Otherwise, you can just look at net shrinkage which offsets all shrinkage by all expansion. The idea of account-level churn is to restrict the ability to offset shrinkage with expansion across accounts, in effect, telling your customer success reps that their job is to, contract by contract, minimize shrinkage and ensure expansion.

[10] "Offset" meaning ARR used to offset shrinkage that ends up neither churn nor upsell.

[11] While this approach works fine for most (inherently single-product) SaaS startups it does not work as well for large multi-product SaaS vendors where the failure of product A might be totally or partially masked by the success of product B. (In our example, I deliberately had all the shrinkage coming from downsell of product A to make that point. The product or general manager for product A should own the churn number that product and be trying to find out why it churned 80 units.)

[12] MRR = monthly recurring revenue = 1/12th of ARR. Because enterprise SaaS companies typically run on an annual business rhythm, I prefer ARR to MRR.

[13] Worse yet, if I churn them out on 5/1 and do succeed in changing their mind, I might need to recognize it as “new ARR” on 6/30, which would also be wrong.

[14] The more popular way of handling this would have been to try and extend the original contract and co-terminate with the upsell in 4Q16, but that doesn’t affect the underlying logic, so let’s just pretend we tried that and it didn’t work for the customer.

[15] Whether you call it a de-booking or bad receivable, Foxtrot was in the ARR base and needs to come out. Unlike the case where the customer has paid for the period but is not using the software (where we should churn it at the end of the contract), in this case the 3Q15 renewal was effectively invalid and we need to remove Foxtrot from the ARR base at some defined number of days past due (e.g., 90) or when we lose hope of collection (e.g., bankruptcy).

[16] I think the smaller you are the more important this correction is to ensure the quality of your numbers. As a company gets bigger, I’d just drop the “+” concept whenever it’s only changing things by a rounding error.

[17] Use NPS surveys for another, more precise, way of measuring happiness. See [7] as well.