A Look at the Tintri S-1

Every now and then I take a dive into an S-1 to see what clears the current, ever-changing bar for going public. After a somewhat rocky IPO process, Tintri went public June 30 after cutting the IPO offering price and has traded flat thus far since then.

Let's read an excerpt from this Business Insider story before taking a look at the numbers.

With the performance of this IPO, the company is now valued at about about $231 million, based on $7.50 a share and its roughly 31 million outstanding shares, (if the IPO's bankers don't buy their optional, additional roughly 1.3 million shares.)

In other words, this IPO killed a good $570 million of the company's value.

In other words, Tintri looks like a "down-round IPO" (or an "IPO of last resort") -- something that frankly almost never happened before the recent mid/late stage private valuation bubble of the past 4 years.

Let's look at some numbers.

Of note:

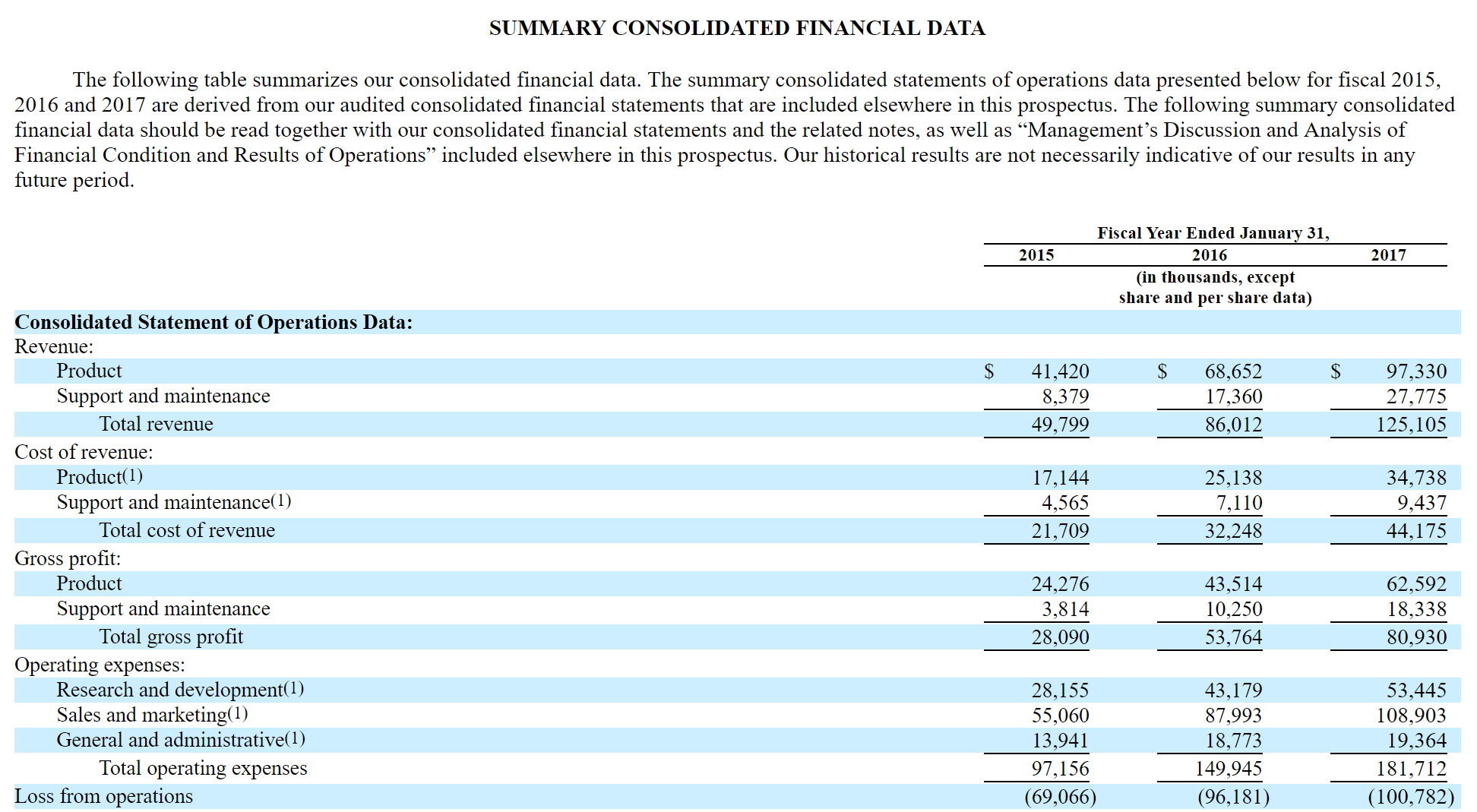

- $125M in FY2017 revenue. (They have scale, but this is not a SaaS company so the revenue is mostly non-recurring, making it easier to get to grow quickly and making the revenue is worth less because only the support/maintenance component of it renews each year.)

- 45% YoY total revenue growth. (On the low side, especially given that they have a traditional license/maintenance model and recognize revenue on shipment.)

- 65% gross margins (Low, but they do seem to sell flash memory hardware as part of their storage solutions.)

- 87% of revenue spent on S&M (High, again particularly for a non-SaaS company.)

- 43% of revenue spent on R&D (High, but usually seen as a good thing if you view the R&D money as well spent.)

- -81% operating margins (Low, particularly for a non-SaaS company.)

- -$70.4M in cashflow from operating activities in 2017 ($17M average quarterly cash burn from operations)

- Incremental S&M / incremental product revenue = 73%, so they're buying $1 worth of incremental (YoY) revenue for an incremental 73 cents in S&M. Expensive but better than some.

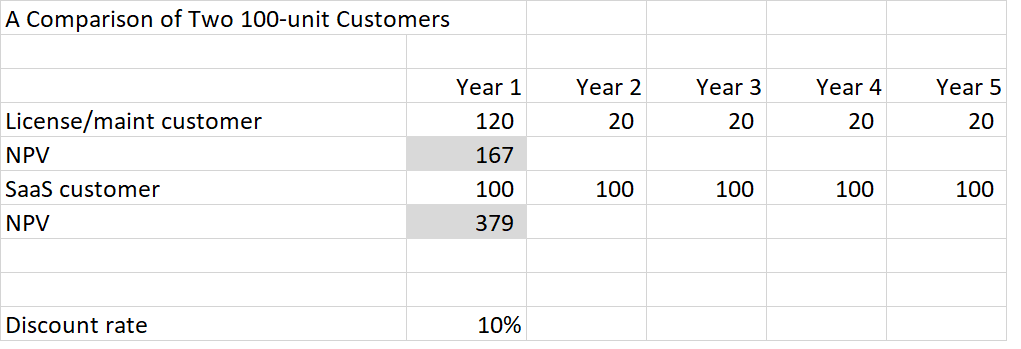

Overall, my impression is of an on-premises (and to a lesser extent, hardware) company in SaaS clothing -- i.e., Tintri's metrics look like a SaaS company, but they aren't so they should look better. SaaS company metrics typically look worse than traditional software companies for two reasons: (1) revenue growth is depressed by the need to amortize revenue over the course of the subscription and (2) subscriptions companies are willing to spend more on S&M to acquire a customer because of the recurring nature of a subscription.

Concretely, if you compare two 100-unit customers, the SaaS customer is worth twice the license/maintenance customer over 5 years.

Moreover, even if Tintri were a SaaS company, it is quite out of compliance with the Rule of 40, that says growth rate + operating margin >= 40%. In Tintri's case, we get -35%, 45% growth plus -81% operating margin, so they're 75 points off the rule.

Other Notes

- 1250+ customers

- 21 of the Fortune 100

- 527 employees as of 1/31/17

- CEO 2017 cash compensation $525K

- CFO 2017 cash compensation $330K

- Issued special retention stock grants in May 2017 that vest in the two years following an IPO

- Did option repricing in May 2017 to $2.28/share down from weighted average exercise price of $4.05.

- $260M in capital raised prior to IPO

- Loans to CFO and CEO to exercise stock options at 1.6% to 1.9% interest in 2013

- NEA 22.7% ownership prior to opening

- Lightspeed 14.5% ownership

- Insight Venture Partners 20.2% ownership

- Silver Lake 20.4% ownership

- CEO 3.8% ownership

- CFO 0.7% ownership

- $48.9M in long-term debt

- $13.8M in 2017 stock-based compensation expense

Overall, and see my disclaimers, but this is one that I'll be passing on.