Quota Over-assignment and Culture

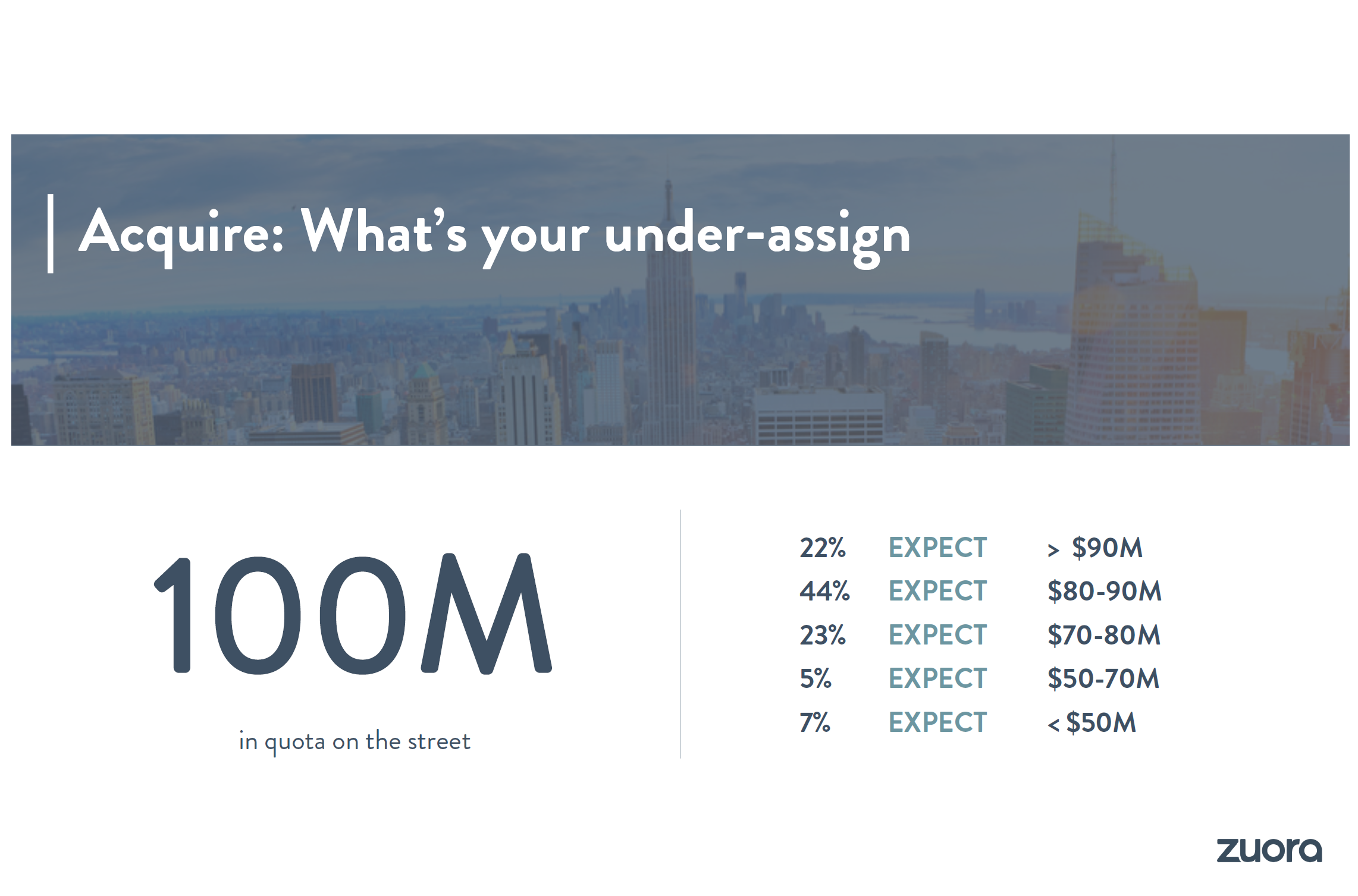

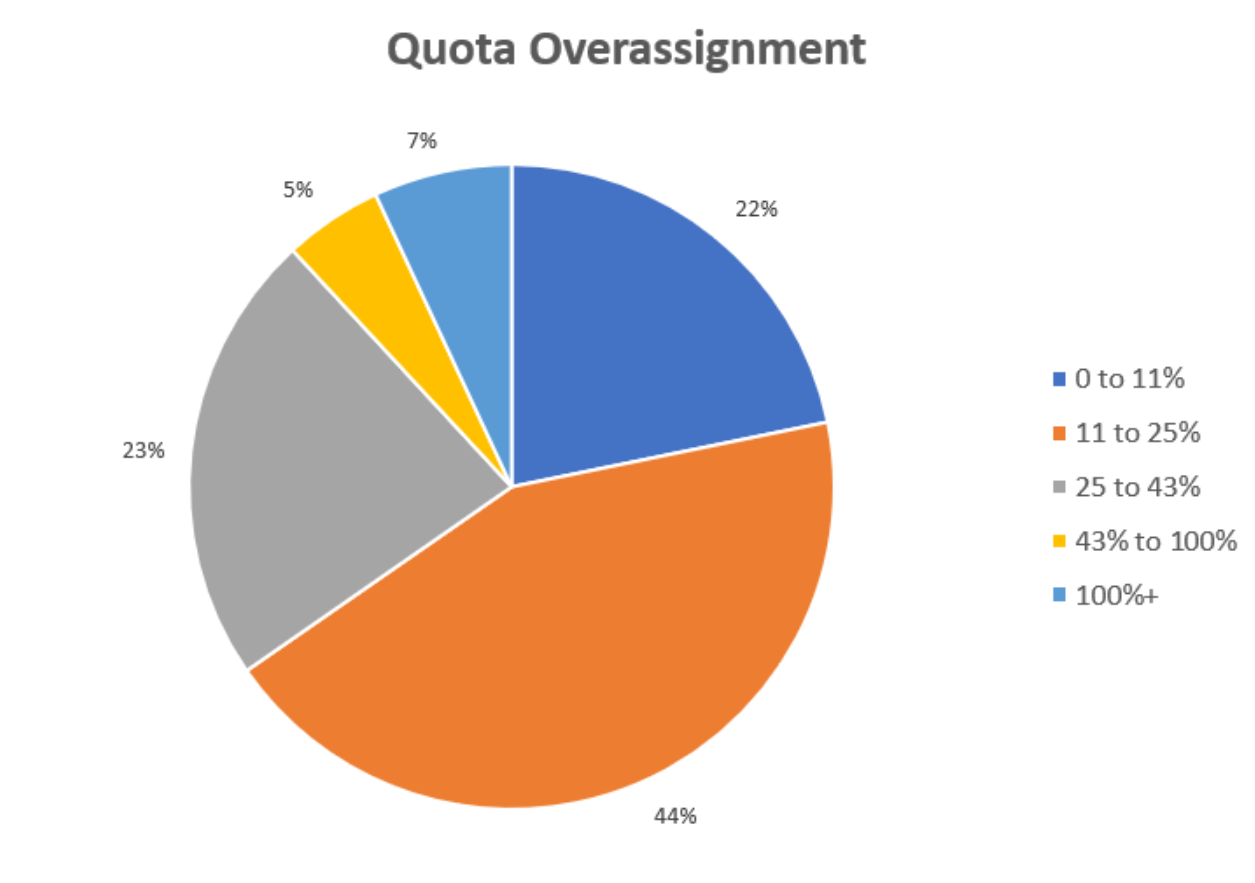

Here's a great slide from the CFO Summit at Zuora's 2017 annual flagship Subscribed event.

Since they talk about this as under-assignment, since people aren't great at flipping fractions in their head, and since I think of this more intuitively as over-assignment, I'm going to invert this and turn it into a pie chart.

So, here you can see that 22% of companies have 0-11% over-assignment of quota, 44% have 11-25% over-assignment, 23% have 25-43%, 5% have 43-100% over-assignment, and 7% have more than 100% over-assignment of quota.

Since this is a pretty broad distribution -- and since this has a real impact on culture, I thought examine this on two different angles: the amount of total cushion and where that cushion lives.

The 0-11% crowd either has a very predictable business model or likes to live dangerously. Since there's not that much cushion to go around, it's not that interesting to discuss who has it. I hope these companies have adequately modeled sales turnover and its effects on quota capacity.

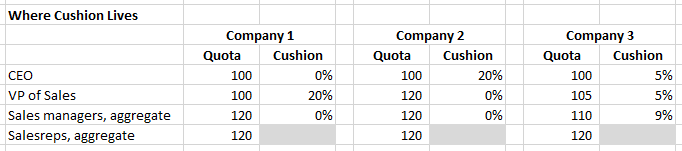

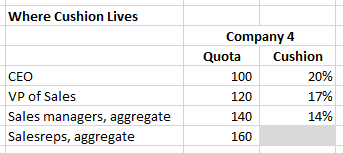

The 11-25% crowd strikes me as reasonable. In my experience, most enterprise software companies run in the 20% range, so they assign 120 units of quota at the salesrep level for an operating plan that requires 100 units of sales. Then the question is who has the cushion? Let's look at three companies.

In company 1, the CEO and VP of Sales are both tied to the same number (i.e., the CEO has no cushion if the VP of Sales misses) and the VP of Sales takes all of the cushion, giving the sales managers none. In company 2, the CEO takes the entire 20% cushion for him/herself, leaving none for either the VP of Sales or the sales managers. In company 3, the cushion is shared with the CEO and VP of Sales each taking a slice, leaving nearly half for the sales managers.

While many might be drawn to company 3, personally, I think the best answer is yet another scenario where the CEO and VP of Sales are both tied to 100, the sales managers to 110, and the aggregate salesrep quota to 120. Unless the CEO has multiple quota-carrying direct reports, it's hard to give the VP of Sales a higher quota than him/herself, so they should tie themselves together and share the 10% cushion from the sales managers who in turn have ~10% cushion relative to their teams.

I think this level of cushion works well if you're building it atop a productivity model that assumes a normal degree of sales turnover (and ramp resets) and are thus using over-assignment simply to handle non-attainment, and not also sales turnover. If you are using over-assignment to handle both, then a higher level of cushion may be needed, which is probably why 22% of companies have 25-43% over-assignment in their sales model.

The shock is the 12% that together have more than 43% over-assignment. Let's ponder for a minute what that might look like in an example with 60% over-assignment.

So think about this for a minute. The VP of Sales can be at 83% of quota, the sales managers on average can be at 71% of quota, and the salesreps can be at 63% of their quota -- and the CEO will still be on plan. The only people hitting their number, making their on-target earnings (OTE), and drinking champagne at the end of the quarter are the CEO and CFO. (And they better drink it in a closet.)

That's why I believe cushion isn't just a math problem. It's a cultural issue. Do you want a "let them eat cake" or a "we're all in this together" culture. The answer to that question should help determine how much cushion you have and where it lives.