The Domo S-1: Does the Emperor Have Clothes?

I preferred Silicon Valley [1] back in the day when companies raised modest amounts of capital (e.g., $30M) prior to an IPO that took 4-6 years from inception, where burn rates of $10M/year looked high, and where $100M raise was the IPO, not one or more rounds prior to it. When cap tables had 1x, non-participating preferred and that all converted to a single class of common stock in the IPO. [2]

How quaint!

These days, companies increasingly raise $200M to $300M prior to an IPO that takes 10-12 years from inception, the burn might look more like $10M/quarter than $10M/year, the cap table loaded up with “structure” (e.g., ratcheting, multiple liquidation preferences). And at IPO time you might end up with two classes common stock, one for the founder with super-voting rights, and one for everybody else.

I think these changes are in general bad:

- Employees get more diluted, can end up alternative minimum tax (AMT) prisoners unable to leave jobs they may be unhappy doing, have options they are restricted from selling entirely or are sold into opaque secondary markets with high legal and transaction fees, and/or even face option expiration at 10 years. (I paid a $2,500 “administrative fee” plus thousands in legal fees to sell shares in one startup in a private transaction.)

- John Q. Public is unable to buy technology companies at $30M in revenue and with a commission of $20/trade. Instead they either have to wait until $100 to $200M in revenue or buy in opaque secondary markets with limited information and high fees.

- Governance can be weak, particularly in cases where a founder exercises directly (or via a nuclear option) total control over a company.

Moreover, the Silicon Valley game changes from “who’s smartest and does the best job serving customers” on relatively equivalent funding to “who can raise the most capital, generate the most hype, and buy the most customers.” In the old game, the customers decide the winners; in the new one, Sand Hill Road tries to, picking them in a somewhat self-fulfilling prophecy.

The Hype Factor

In terms of hype, one metric I use is what I call the hype ratio = VC / ARR. On the theory that SaaS startups input venture capital (VC) and output two things -- annual recurring revenue (ARR) and hype -- by analogy, heat and light, this is a good way to measure how efficiently they generate ARR.

The higher the ratio, the more light and the less heat. For example, Adaptive Insights raised $175M and did $106M in revenue [3] in the most recent fiscal year, for a ratio of 1.6. Zuora raised $250M to get $138M in ARR, for a ratio of 1.8. Avalara raised $340M to $213M in revenue, for a ratio of 1.6.

By comparison, Domo's hype ratio is 6.4. Put the other way, Domo converts VC into ARR at a 15% rate. The other 85% is, per my theory, hype. You give them $1 and you get $0.15 of heat, and $0.85 of light. It's one of the most hyped companies I've ever seen.

As I often say, behind every "marketing genius" is a giant budget, and Domo is no exception [4].

Sometimes things go awry despite the most blue-blooded of investors and the greenest of venture money. Even with funding from the likes of NEA and Lightspeed, Tintri ended up a down-round IPO of last resort and now appears to be singing its swan song. In the EPM space, Tidemark was the poster child for more light than heat and was sold in what was rumored to be fire sale [5] after raising over $100M in venture capital and having turned that into what was supposedly less than $10M in ARR, an implied hype ratio of over 10.

The Top-Level View on Domo

Let's come back and look at the company. Roughly speaking [6], Domo:

- Has nearly $700M in VC invested (plus nearly $100M in long-term debt).

- Created a circa $100M business, growing at 45% (and decelerating).

- Burns about $150M per year in operating cash flow.

- Will have a two-class common stock system where class A shares have 40x the voting rights of class B, with class A totally controlled by the founder. That is, weak governance.

Oh, and we’ve got a highly unprofitable, venture-backed startup using a private jet for a bit less than $1M year [7]. Did I mention that it’s leased back from the founder? Or the $300K in catering from a company owned by the founder and his brother. (Can't you order lunch from a non-related party?)

As one friend put it, "the Domo S-1 is everything that's wrong with Silicon Valley in one place: huge losses, weak governance, and now modest growth."

Personally, I view Domo as the Kardashians of business intelligence – famous for being famous. While the S-1 says they have 85 issued patents (and 45 applications in process), does anyone know what they actually do or what their technology advantage is? I’ve worked in and around BI for nearly two decades – and I have no idea.

Maybe this picture will help.

Uh, not so much.

The company itself admits the current financial situation is unsustainable.

If other equity or debt financing is not available by August 2018, management will then begin to implement plans to significantly reduce operating expenses. These plans primarily consist of significant reductions to marketing costs, including reducing the size and scope of our annual user conference, lowering hiring goals and reducing or eliminating certain discretionary spending as necessary

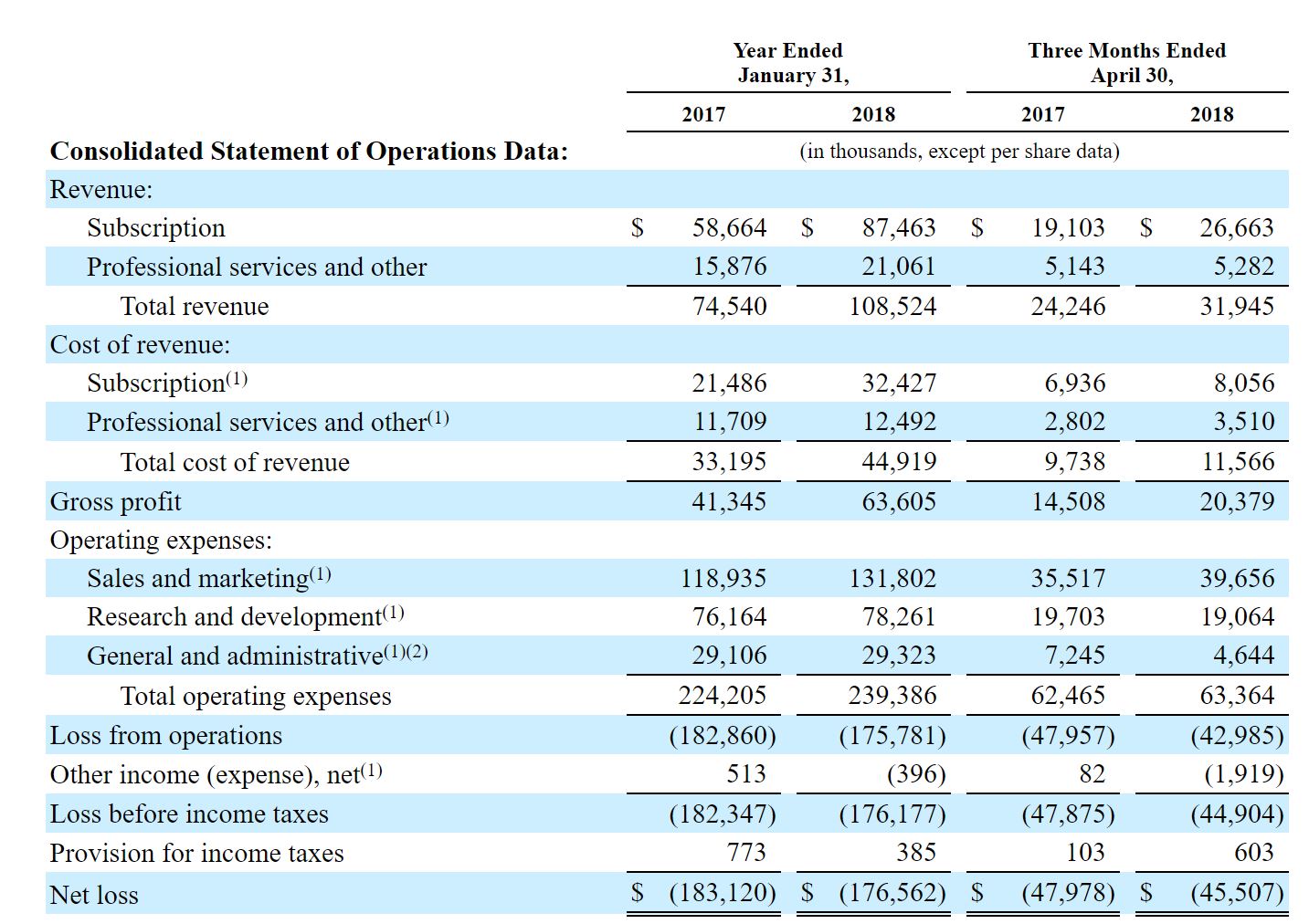

A Top-to-Bottom Skim of the S-1So, with that as an introduction, let's do a quick dig through the S-1, starting with the income statement:

Of note:

- 45% YoY revenue growth, slow for the burn rate.

- 58% blended gross margins, 63% subscription gross margins, low.

- S&M expense of 121% of revenue, massive.

- R&D expense of 72% of revenue, huge.

- G&A expense of 29% of revenue, not even efficient there.

- Operating margin of -162%, huge.

Other highlights:

- $803M accumulated deficit. Stop, read that number again and then continue.

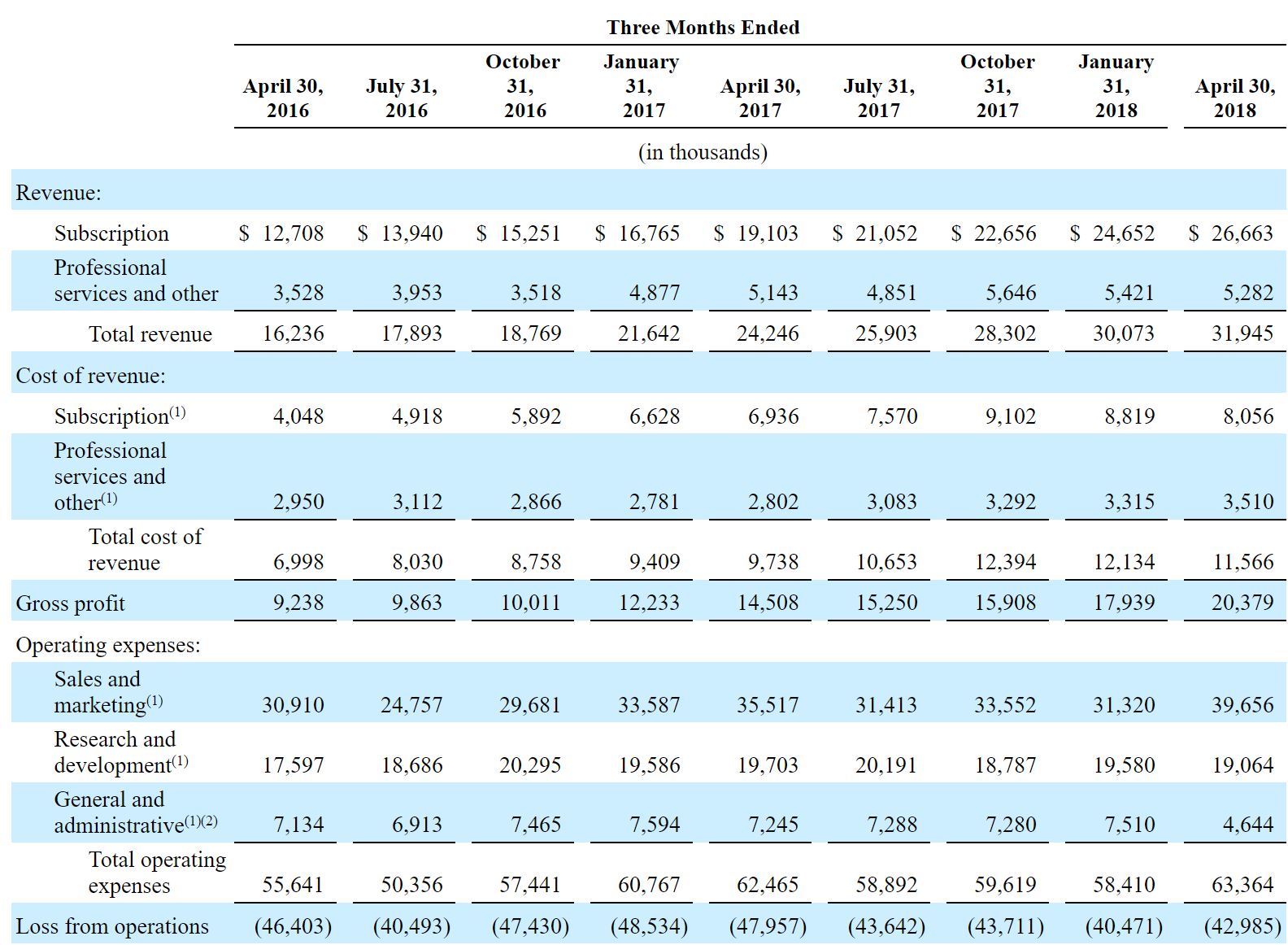

- Decelerating revenue growth, 45% year over year, but only 32% Q1 over Q1.

- Cashflow from operations around -$150M/year for the past two years. Stunning.

- 38% of customers did multi-year contracts during FY18. Up from prior year.

- Don't see any classical SaaS unit economics, though they do a 2016 cohort analysis arguing contribution margin from that cohort of -196%, 52%, 56% over the past 3 years. Seems to imply a CAC ratio of nearly 4, twice what is normally considered on the high side.

- Cumulative R&D investment from inception of $333.9M in the platform.

- 82% revenues from USA in FY18.

- 1,500 customers, with 385 having revenues of $1B+.

- Believe they are <4% penetrated into existing customers, based on Domo users / total headcount of top 20 penetrated customers.

- 14% of revenue from top 20 customers.

- Three-year retention rate of 186% in enterprise customers (see below). Very good.

- Three-year retention rate of 59% in non-enterprise customers. Horrific. Pay a huge CAC to buy a melting ice cube. (Only the 1-year cohort is more than 100%.)

As of January 31, 2018, for the cohort of enterprise customers that licensed our product in the fiscal year ended January 31, 2015, the current ACV is 186% of the original license value, compared to 129% and 160% for the cohorts of enterprise customers that subscribed to our platform in the fiscal years ended January 31, 2016 and 2017, respectively. For the cohort of non-enterprise customers that licensed our product in the fiscal year ended January 31, 2015, the current ACV as of January 31, 2018 was 59% of the original license value, compared to 86% and 111% for the cohorts of non-enterprise customers that subscribed to our platform in the fiscal years ended January 31, 2016 and 2017, respectively.

- $12.4M in churn ARR in FY18 which strikes me as quite high coming off subscription revenues of $58.6M in the prior year (21%). See below.

Our gross subscription dollars churned is equal to the amount of subscription revenue we lost in the current period from the cohort of customers who generated subscription revenue in the prior year period. In the fiscal year ended January 31, 2018, we lost $12.4 million of subscription revenue generated by the cohort in the prior year period, $5.0 million of which was lost from our cohort of enterprise customers and $7.4 million of which was lost from our cohort of non-enterprise customers.

- What appears to be reasonable revenue retention rates in the 105% to 110% range overall. Doesn't seem to foot to the churn figure about. See below:

For our enterprise customers, our quarterly subscription net revenue retention rate was 108%, 122%, 116%, 122% and 115% for each of the quarters during the fiscal year ended January 31, 2018 and the three months ended April 30, 2018, respectively. For our non-enterprise customers, our quarterly subscription net revenue retention rate was 95%, 95%, 99%, 102% and 98% for each of the quarters during the fiscal year ended January 31, 2018 and the three months ended April 30, 2018, respectively. For all customers, our quarterly subscription net revenue retention rate was 101%, 107%, 107%, 111% and 105% for each of the quarters during the fiscal year ended January 31, 2018 and the three months ended April 30, 2018, respectively.

- Another fun quote and, well, they did take about the cash it takes to build seven startups.

Historically, given building Domo was like building seven start-ups in one, we had to make significant investments in research and development to build a platform that powers a business and provides enterprises with features and functionality that they require.

- Most customers invoiced on annual basis.

- Quarterly income statements, below.

- $72M in cash as of 4/30/18, about 6 months worth at current burn.

- $71M in "backlog," multi-year contractual commitments, not prepaid and ergo not in deferred revenue. Of that $41M not expected to be invoiced in FY19.

- Business description, below. Everything a VC could want in one paragraph.

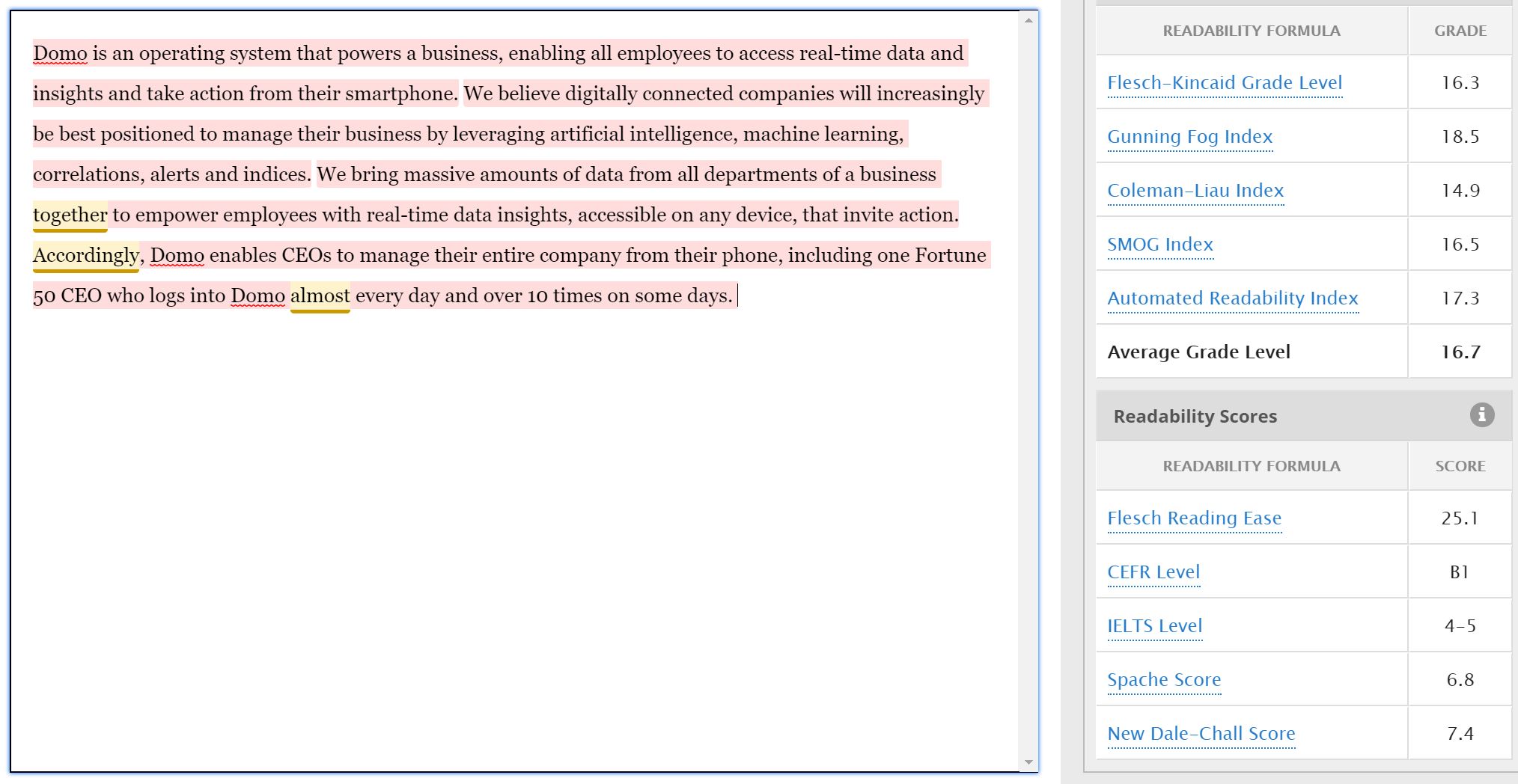

Domo is an operating system that powers a business, enabling all employees to access real-time data and insights and take action from their smartphone. We believe digitally connected companies will increasingly be best positioned to manage their business by leveraging artificial intelligence, machine learning, correlations, alerts and indices. We bring massive amounts of data from all departments of a business together to empower employees with real-time data insights, accessible on any device, that invite action. Accordingly, Domo enables CEOs to manage their entire company from their phone, including one Fortune 50 CEO who logs into Domo almost every day and over 10 times on some days.

- Let's see if a computer could read it any better than I could. Not really.

- They even have Mr. Roboto to help with data analysis.

Through Mr. Roboto, which leverages machine learning algorithms, artificial intelligence and predictive analytics, Domo creates alerts, detects anomalies, optimizes queries, and suggests areas of interest to help people focus on what matters most. We are also developing additional artificial intelligence capabilities to enable users to develop benchmarks and indexes based on data in the Domo platform, as well as automatic write back to other systems.

- 796 employees as of 4/30/18, of which 698 are in the USA.

- Cash comp of $525K for CEO, $450K for CFO, and $800K for chief product officer

- Pre-offering it looks like founder Josh James owns 48.9M shares of class A and 8.9M shares of class B, or about 30% of the shares. With the 40x voting rights, he has 91.7% of the voting power.

Does the Emperor Have Any Clothes?One thing is clear. Domo is not "hot" because they have some huge business blossoming out from underneath them. They are "hot" because they have raised and spent an enormous amount of money to get on your radar.

Will they pull off they IPO? There's a lot not to like: the huge losses, the relatively slow growth, the non-enterprise retention rates, the presumably high CAC, the $12M in FY18 churn, and the 40x voting rights, just for starters.

However, on the flip side, they've got a proven charismatic entrepreneur / founder in Josh James, an argument about their enterprise customer success, growth, and penetration (which I've not had time to crunch the numbers on), and an overall story that has worked very well with investors thus far.

While the Emperor's definitely not fully dressed, he's not quite naked either. I'd say the Domo Emperor's donning a Speedo -- and will somehow probably pull off the IPO parade.

###

Notes

[1] Yes, I know they're in Utah, but this is still about Silicon Valley culture and investors.

[2] For definitions and frequency of use of various VC terms, go to the Fenwick and West VC survey.

[3] I'll use revenue rather than trying to get implied ARR to keep the math simple. In a more perfect world, I'd use ARR itself and/or impute it. I'd also correct for debt and a cash, but I don't have any MBAs working for me to do that, so we'll keep it back of the envelope.

[4] You can argue that part of the "genius" is allocating the budget, and it probably is. Sometimes that money is well spent cultivating a great image of a company people want to buy from and work at (e.g., Salesforce). Sometimes, it all goes up in smoke.

[5] Always somewhat truth-challenged, Tidemark couldn't admit they were sold. Instead, they announced funding from a control-oriented private equity firm, Marlin Equity Partners, as a growth investment only a year later be merged into existing Marlin platform investment Longview Solutions.

[6] I am not a financial analyst, I do not give buy/sell guidance, and I do not have a staff working with me to ensure I don’t make transcription or other errors in quickly analyzing a long and complex document. Readers are encouraged to go the S-1 directly. Like my wife, I assume that my conclusions are not always correct; readers are encouraged to draw their own conclusions. See my FAQ for complete disclaimer.

[7] $900K, $700K, and $800K run-rate for FY17, FY18, and 1Q19 respectively.