My Final Verdict on Multi-Year, Prepaid Deals

(Revised 5/4/19, 10:41 AM.)

After years of experience with and thinking about multi-year, prepaid SaaS deals, my mental jury is back in the box and the verdict is in: if you're a startup that is within my assumption set below, don't do them.

Before jumping in, let me first define precisely what I mean by multi-year, prepaid deals and second, detail the assumptions behind my logic in response to some Twitter conversations I've had this morning about this post.

What do I Mean by Multi-Year Prepaid Deals?

While there are many forms of "multi-year prepaid deals," when I use the term I am thinking primarily of a three-year agreement that is fully prepaid. For example, if a customer's ARR cost is 100 units for a one-year deal, you might approach them saying something akin to:

By default, our annual contracts have a 10% annual increase built in [1]. If you sign and prepay a three-year agreement, i.e., pay me 300 units within 60 days, then I will lock you in at the 100 units per year price.

Some people didn't know these kinds of deals were possible -- they are. In my experience, particularly for high-consideration purchases (where the customer has completed a thorough evaluation and is quite sure the system will work), a fairly high percentage of buyers will engage in this conversation. (In a world where companies have a lot of cash, a 10% return is a lot better than bank interest.)

Multi-year prepaid deals can take other forms as well:

- The duration can vary: I've seen anything from 2 to 7 years.

- The contract duration and the prepaid duration can decouple: e.g., a five-year deal where the first three years are prepaid.

But, to make it simple, just think of a three-year fully prepaid deal as the canonical example.

What are My Underlying Assumptions?

As several readers pointed out, there are some very good reasons to do multi-year prepaid deals [11]. Most of all, they're a financial win/win for both vendor and customer: the customer earns a higher rate of return than bank interest and the vendor gets access to capital at a modest cost.

If you're bootstrapping a company with your own money, have no intention to raise venture capital, and aren't concerned about complicating an eventual exit to a private equity (PE) or strategic acquirer, then I'd say go ahead and do them if you want to and your customers are game.

However, if you are venture-backed, intend to raise one or more additional rounds before an exit, and anticipate selling to either a strategic or private equity acquirer, then I'd say you should make yourself quite familiar with the following list of disadvantages before building multi-year prepaid deals into your business model.

Why do I Recommend Avoiding Multi-Year Prepaid Deals?

In a phrase, it's because they're not the norm. If you want to raise money from (and eventually sell to) people who are used to SaaS businesses that look a certain way -- unless you are specifically trying to disrupt the business model -- then you should generally do things that certain way. Multi-year prepaid deals complicate numerous things and each of those complications will be seen not as endemic to the space, but as idiosyncratic to your company.

Here's the list of reasons why you should watch out. Multi-year prepaid deals:

- Are not the norm, so they raise eyebrows among investors and can backfire with customers [2].

- Complexify SaaS metrics. SaaS businesses are hard enough to understand already. Multi-year deals make metrics calculation and interpretation even more complicated. For example, do you want to argue with investors that your CAC payback period is not 18 months, but one day? You can, but you'll face a great risk of "dying right" in so doing. (And I have done so on more than one occasion [3]).

- Amplify churn rates. An annual renewal rate [4] of 90% is equivalent to a three-year renewal rate of 72%. But do you want to argue that, say, 79% is better than 90% [5] or that you should take the Nth root of N-year renewal rates to properly compare them to one-year rates? You can, but real math is all too often seen as company spin, especially once eyebrows are already raised.

- Confuse churn rates. In a world where investors generally fear complexity, do you want to have to calculate churn rates on both an available-to-renew (ATR) and overall ARR pool basis and then explain the difference? I don't.

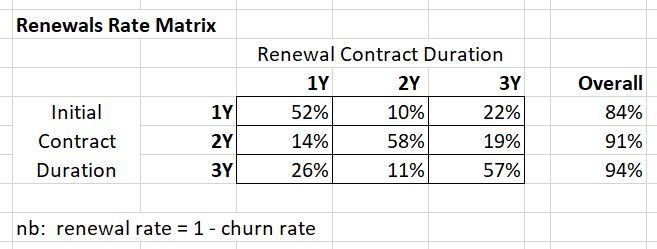

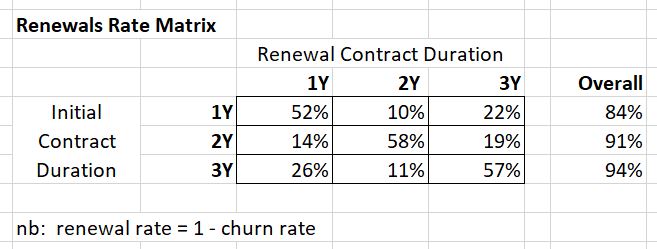

- Turn your renewals rate into a renewals matrix. Technically speaking, if you're doing a mix of one, two, and three-year deals, then your renewal rate isn't a single rate at all, but a matrix. Do you want to explain that to investors?

- Tee you up for price knock-off at sales time. Some buyers, particularly those in private equity (PE), will look at the relatively large long-term deferred revenue balance as "cashless revenue" and try to deduct the cost of it from an acquisition price [6]. Moreover, if not discussed up front, someone might try to knock it off what you thought was a final number.

- Can reduce value for strategic acquirers. Under today's rules, for reasons that I don't entirely understand, deferred revenue seems to get written off (and thus never recognized) in a SaaS acquisition. So, ceteris paribus, an acquirer would greatly prefer non-prepaid TCV (which it will get to recognize over time) to deferred revenues (which it won't) [7].

- Can give pause to strategic acquirers. Anything that might cause the acquirer to need to start release pro forma financials has the potential to scare them off, particularly one with otherwise pristine financial statements. For example, having to explain why revenue from a recently acquired startup is shrinking year-over-year might do precisely that [8].

- Can "inflate" revenues. Under ASC 606, multi-year, prepaid deals are seen as significant financing events, so -- if I have this correct -- revenue will exceed the cash received [9] from the customer as interest expense will be recorded and increase the amount of revenue. Some buyers, particularly PE ones, will see this as another form of cashless revenue and want to deflate your financials to account for it since they are not primarily concerned with GAAP financials, but are more cash-focused.

- Will similarly inflate remaining performance obligation (RPO). SaaS companies are increasingly releasing a metric called RPO which I believe is supposed to be a more rigorous form of what one might call "remaining TCV (total contract value)" -- i.e., whether prepaid or not, the value of remaining obligations undertaken in the company's current set of contracts. If this is calculated on a GAAP basis, you're going to have the same inflation issue as with revenues when multi-year, prepaid deals are involved. For example, I think a three-year 100-unit deal done with annual payments will show up as 200 units of RPO but the same deal done a prepaid basis will show up as 200-something (e.g., 210, 220) due to imputed interest.

- Impede analysis of billings. If you want to go public or get acquired by a public company, financial analysts are going to focus on a metric called calculated billings [10] which is equal to revenue plus the change in deferred revenue for a given time period. For SaaS purist companies (i.e., those that do only annual contracts with one-year prepays), calculated billings is actually a pretty good measure of new sales. Multi-year prepays impede analysis of billings because deferred revenue ends up a mishmash of deals of varying lengths and is thus basically impossible to interpret [11]. This could preclude an acquisition by a SaaS purist company [12].

More than anything, I think when you take these factors together, you can end up with complexity fatigue which ultimately takes you back to whether it's a normal industry practice. If it were, people would just think, "that's the complexity endemic in the space." If it's not, people think, "gosh, it's just too darn hard to normalize this company to the ones in our portfolio [13] and my head hurts."

Yes, there are a few very good reasons to do multi-year, prepaid deals [14], but overall, I'd say most investors and acquirers would prefer if you just raised a bit more capital and didn't try to finance your growth using customer prepayments. In my experience, the norm in enterprise software is increasingly converging to three-year deals with annual payments which provide many of the advantages of multi-year deals without a lot of the added complexity [15].

# # #

Notes

[1] While 10% is indeed high, it makes the math easier for the example (i.e., the three-year cost is 331 vs. 300). In reality, I think 5-6% is more reasonable, though it's always easier to reduce something than increase it in a negotiation.

[2] Especially if your competition primes them by saying -- "those guys are in financial trouble, they need cash, so they're going to ask you for a multi-year, prepaid deal. Mark my words!"

[3] Think: "I know the formula you're using says '18 months' but I'm holding an invoice (or, if you wait 30 days, check) in my hand for more than the customer acquisition cost." Or, "remember from b-school that payback periods are supposed to measure risk, no return, and to do so by measuring how long your money is on the table." Or, "the problem with your formula is you're producing a continuous result in a world where you actually only collect modulo 12 months -- isn't that a problem for a would-be 'payback' metric?"

[4] Renewal rate = 1 - churn rate

[5] That is, that a 79% three-year rate is ergo better than a one-year 90% renewal rate.

[6] Arguing that while the buyer will get to recognize the deferred revenue over time that the cash has already been collected, and ergo that the purchase price should be reduced by the cost of delivering that revenue, i.e., (COGS %) * (long-term deferred revenue).

[7] Happily, the deferred revenue write-down approach seems to be in the midst of re-evaluation.

[8] If the acquired company does a high percentage of multi-year, prepaid deals and you write off its deferred revenue, it will certainly reduce its apparent growth rate and possibly cause it to shrink on a year-over-year basis. What was "in the bag revenue" for the acquired company gets vaporized for the acquirer.

[9] Or our other subsidiaries, for a strategic acquirer.

[10] Known either as billings or calculated billings. I prefer the latter because it emphasizes that it's not a metric that most companies publish, but one commonly derived by financial analysts.

[11] We are testing the limits of my accounting knowledge here, but I suppose if deferred revenue is split into current and long-term you might still be able to get a reasonable guestimate for new ARR sales by calculating billings based only on current, but I'm not sure that's true and worry that the constant flow from long-term to current deferred revenue will impede that analysis.

[12] A purist SaaS company -- and they do exist -- would actually see two problems. First, potential year-over-year shrinkage due to the write-down discussed in footnote [7]. Second, they'd face a dilemma in choosing between the risk associated with immediately transitioning the acquired company's business to annual-only and the potential pollution of its otherwise pristine deferred revenue if they don't.

[13] Minute 1:28 of the same video referenced in the prior link.

[14] Good reasons to do multi-year, prepaid deals include: (a) they are arguably a clever form of financing using customer money, (b) they tend to buy you a second chance if a customer fails in implementation (e.g., if you've failed 9 months into a one-year contract, odds are you won't try again -- with a three-year, prepay you might well), (c) they are usually a financing win/win for both vendor and customer as the discount offered exceeds the time value of money.

[15] You do get one new form of complexity which is whether to count payments as renewals, but if everyone is doing 3-year, annual payment deals then a norm will be established.