Are We Due for a SaaSacre?

I was playing around on the enterprise comps [1] section of Meritech's website today and a few of the charts I found caught my attention. Here's the first one, which shows the progression of the EV/NTM revenue multiple [2] for a set of 50+ high-growth SaaS companies over the past 15 or so years [3].

While the green line (equity-value-weighted [4]) is the most dramatic, the one I gravitate to is the blue line: the median EV/NTM revenue multiple. Looking at the blue line, you can see that while it's pretty volatile, eyeballing it, I'd say it normally runs in the range between 5x and 10x. Sometimes (e.g., 2008) it can get well below 5x. Sometimes (e.g., in 2013) it can get well above 10x. As of the last data point in this series (7/14/20) it stood at 13.8x, down from an all-time high of 14.9x. Only in 2013 did it get close to these levels.

If you believe in regression to the mean [5], that means you believe the multiples are due to drop back to the 5-10 range over time. Since mean reversion can come with over-correction (e.g., 2008, 2015) it's not outrageous to think that multiples could drop towards the middle or bottom of that range, i.e., closer to 5 than 10 [6].

Ceteris paribus, that means the potential for a 33% to 66% downside in these stocks. It also suggests that -- barring structural change [7] that moves baseline multiples to a different level -- the primary source of potential upside in these stocks is not continued multiple expansion, but positive NTM revenue surprises [8].

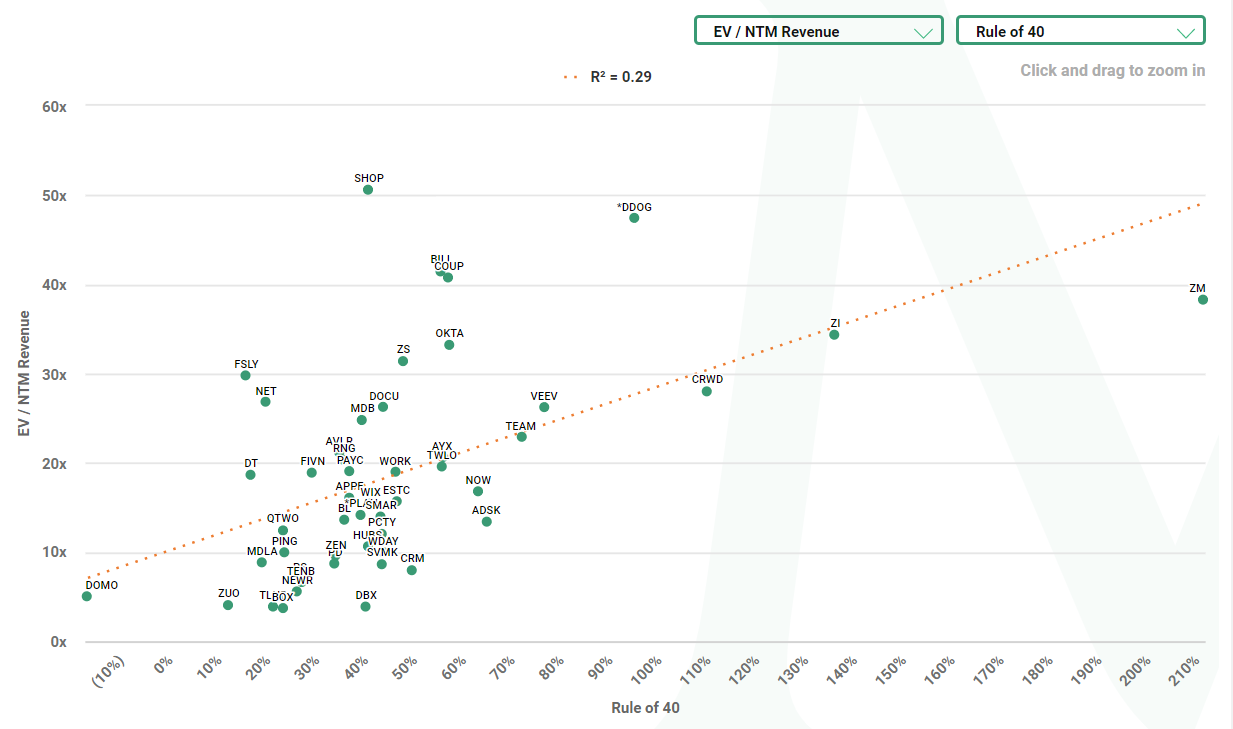

I always love Rule of 40 charts, so the next fun chart that caught my eye was this one.

While this chart doesn't speak to valuations over time, it does speak to the relationship between a company's Rule of 40 Score and its EV/NTM revenue multiple. Higher valuations primarily just shift the Y axis, as they have done here, uplifting the maximum Y-value by nearly three times since I last blogged about such a chart [9]. The explanatory power of the Rule of 40 in explaining valuation multiple is down since I last looked, by about half from an R-squared of 0.58 to 0.29. Implied ARR growth alone has a higher explanatory power (0.39) than the Rule of 40.

To me, this all suggests that in these frothy times, the balance of growth and profit (which is what Rule of 40 measures) matters less than other factors, such as growth, leadership, scarcity value and hype, among others.

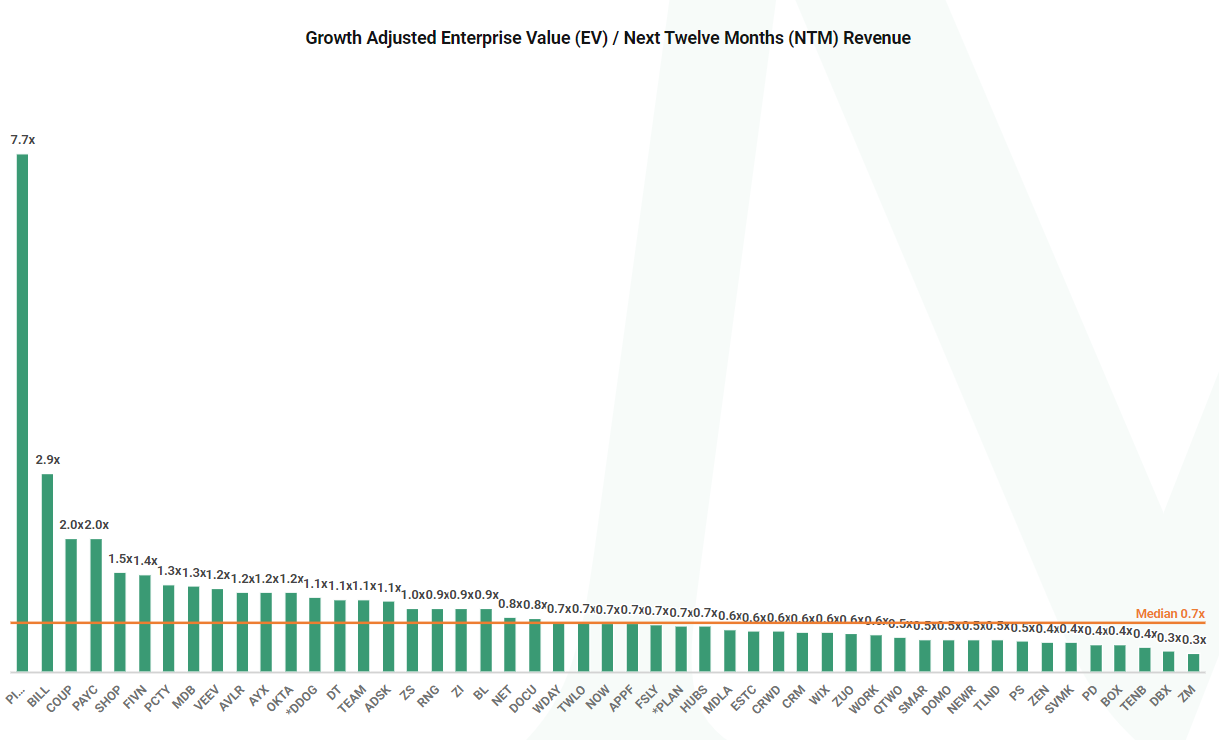

Finally, to come back to valuation multiples, let's look at a metric that's new to me, growth-adjusted EV/R multiples.

I've seen growth-adjusted price/earnings ratios (i.e., PEG ratios) before, but I've not seen someone do the same thing with EV/R multiples. The basic idea is to normalize for growth in looking at a multiple, such as P/E or -- why not -- EV/R. For example, Coupa, trading at (a lofty) 40.8x EV/R is growing at 21%, so divide 40.8 by 21 to get 1.98x. Zoom, by comparison looks to be similarly expensive at 38.3x EV/R but is growing at 139%, so divide 38.3 by 139 to get 0.28x, making Zoom a relative bargain when examined in this light [10].

This is a cool metric. I like financial metrics that normalize things [11]. I'm surprised I've not seen someone do it to EV/R ratios before. Here's an interesting observation I just made using it:

- To the extent a "cheap" PE firm might pay 4x revenues for a company growing 20%, they are buying in at a 0.2 growth-adjusted EV/R ratio.

- To the extent a "crazy" VC firm might pay 15x revenues for a company growing at 75%, they are buying in at a 0.2 growth-adjusted EV/R ratio.

- The observant reader may notice they are both paying the same ratio for growth-adjusted EV/R. Given this, perhaps the real difference isn't that one is cheap and the other free-spending, but that they pay the same for growth while taking on very different risk profiles.

The other thing the observant reader will notice is that in both those pseudo-random yet nevertheless realistic examples, the professionals were paying 0.2. The public market median today is 0.7.

See here for the original charts and data on the Meritech site.

Disclaimer: I am not a financial analyst and do not make buy/sell recommendations. I own positions in a wide range of public and private technology companies. See complete disclaimers in my FAQ.

# # #

Notes [1] Comps = comparables.

[2] EV/NTM Revenue = enterprise value / next twelve months revenue, a so-called "forward" multiple.

[3] Per the footer, since Salesforce's June, 2004 IPO.

[4] As are most stock indexes. See here for more.

[5] And not everybody does. People often believe "this time it's different" based on irrational folly, but sometimes this time really is different (e.g., structural change). For example, software multiples have structurally increased over the past 20 years because the underlying business model changed from one-shot to recurring, ergo increasing the value of the revenue.

[6] And that's not to mention external risk factors such as pandemic or election uncertainty. Presumably these are already priced into the market in some way, but changes to how they are priced in could result in swings either direction.

[7] You might argue a scarcity premium for such leaders constitutes a form of structural change. I'm sure there are other arguments as well.

[8] To the extent a stock price is determined by some metric * some multiple, the price goes up either due to increasing the multiple (aka, multiple expansion) or increasing the metric (or both).

[9] While not a scientific way to look at this, the last time I blogged on a Rule of 40 chart, the Y axis topped out at 18x, with the highest data point at nearly 16x. Here the Y axis tops out at 60x, with the highest data point just above 50x.

[10] In English, to the extent you're paying for EV/R multiple in order to buy growth, Zoom buys you 7x more growth per EV/R point than Coupa.

[11] As an operator, I don't like compound operational metrics because you need to un-tangle them to figure out what to fix (e.g., is a broken LTV/CAC due to LTV or CAC?), but as investor I like compound metrics as much as the next person.