Kellblog Predictions for 2023

Complete version, see note [1] for details.

Yikes, I'm a few weeks later than usual and now slipping into February, so let’s jump right into our ninth annual predictions post before it's too late to publish. A quick reminder that I do these for fun and fun alone. See my FAQ for my terms, disclosures, disclaimers, and the like.

Kellblog 2022 Predictions Review

Let’s start with a review of last year’s predictions which, as it turns out, were pretty good.

Covid transitions from pandemic to endemic. Hit. We can debate the semantics. Epidemiologists would surely differ. And the billionaires at Davos still don't treat it like a cold. But nevertheless, I think people now generally treat Covid as endemic.

Web3 hype peaks. Hit. I don’t think I’ve ever nailed a prediction harder than this one. My new#boi weeps for its loss in financial, if not aesthetic, value.

Disruptors get disrupted. Hit. The point here was that just as we become our parents, that Salesforce becomes Oracle, Nvidia becomes Intel, and so on. This is more the ebb and flow of a natural cycle than a specific prediction -- but given Salesforce’s rather dismal year end, I’ll give myself a hit.

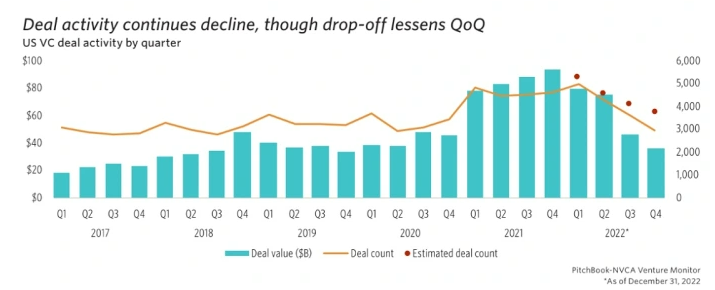

VC continues to flow. Miss. Well, while VC funding was down dramatically in 2022 compared to 2021, but remember that 2021 funding was at all all-time high.

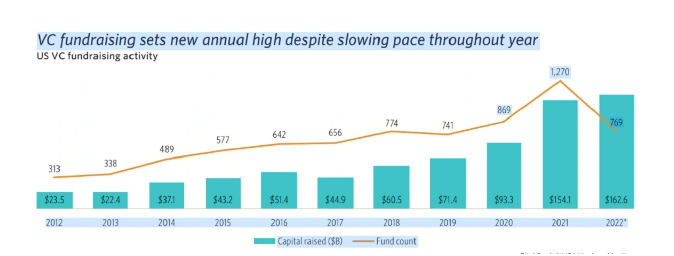

The more interesting point is that all this didn’t slow VC fundraising, which hit a record high in 2022.

Going forward, while VCs clearly have dry powder, what's unclear is their willingness to invest it. High-quality companies will still be financed, if on less stratospheric terms. Those delivering average performance may find themselves with water, water everywhere, but not a drop to drink. Some believe that capital won't flow again until after an extinction-level event for startups in 2023/2024.

-

The metaverse remains meta. Hit. Big companies periodically catch self-boredom-itis and attempt to cure it with top-down pivots, dreamed up in corporate offsites with no regard for existing customers and no recollection of the organic, bottom-up processes that helped them become big in the first place. IBM Watson. Salesforce Chatter. Oracle Network Computer. Informatica Analytic Applications. BusinessObjects Sundance. Some companies treat these as publicity stunts, talking a big vision, but not really investing. Others get confused, believe their own marketing, and bet the ranch. Meta is in that situation: customers don’t care, the market doesn’t look attractive, and key employees are leaving. Yet on they plow. A+ commitment to a C+ strategy.

-

PLG momentum builds. Hit. I think PLG momentum built -- and peaked -- in 2022. Former Redpoint VC Tomasz Tunguz pointed out that product-led growth (PLG) firms are less profitable than sales-led growth firms, poking a hole in the "product sells itself" myth, and clouding dreams of liberation from costly S&M departments. (What drove people to the trial again, anyway?) PLG is a good strategy for certain categories, but VCs have a tendency, with all good intentions, to ram strategies down the throats of portfolio companies. As it turns out, PLG is like Nebraska: "honestly, it's not for everyone."

7. Year of the privacy vault. Partial. While it's hard to back this with data, I believe both Okta and Hashicorp are doing well with their secrets vaults, which continues to validate the vault design pattern. I

remain excited about vaults as applied to privacy (for all the reasons I detailed last year) and my friends at continued to make great progress with their privacy vault and the of it. What if privacy had an API? Well, it should.8. MSDS is the new MBA. Partial. I don't know how to easily measure this (irony not lost), so the scoring is entirely subjective. The in-hindsight obvious thing I hadn't seen coming was the integration of the two -- e.g., CMU's Tepper school offers both an MBA in Business Analytics and an MS in Business Analytics, as do many others. So the new MBA just might be an MBA in Business Analytics or an MSDS.

9. Get ready for social impact. Partial. I was right about the things that concern younger generations. I was wrong to the extent that those things now matter somewhat less as the downturn transfers power from employees to employers. Social change isn't just about what people believe, it's about their power to get it. This is not to stay the new agenda will be completely ignored, but simply that change will come more slowly because the balance of power has shifted.

10. The rise of causal inference. Hit. I continue to believe that causal inference will be to the 2020s what data science was to the 2010s. Read The Book of Why to learn more. Or take this causal data science course on Udemy.

Kellblog Predictions for 2023

With that warm up, here are my predictions for 2023.

- The great pendulum of Silicon Valley swings back. If you look at Silicon Valley over long periods of time, you see a series of pendulums that swing over decades, all loosely coupled to a great pendulum. In 2022, that great (fka master) pendulum started to reverse its course and that will continue in 2023.

While Davos, Main Street, and Wall Street may differ on scale and scope, everyone agrees that the economy is turning. On Sand Hill Road, they're analyzing softening customer demand. The interesting part is how this will drive six sub-pendulums in 2023.

- The valuation pendulum: 10x is the new 20x, flat is the new up. That means a lot of companies need to double their size in order to earn their last-round valuation. Some have raised enough and/or spent sufficiently little that they can do so on existing cash. Others are not so fortunate. Runway extension is the watchword of the day.

- The structure pendulum: it's back. One way to maintain a flat headline valuation is to raise money with what’s commonly called structure. Structure generally means financing terms, such as multiple liquidation preferences or participation (definitions here), that favor new investors over existing investors and the common stockholders in a liquidation. During boom times, structure falls out of favor. During slowdowns, structure, and the so-called dirty term sheets that propose it, come back. Caveat emptor. Think hard and model multiple scenarios before doing a structured round -- a dilutive downround or a clean company sale just might drive more long-term value.

- The growth vs. profit pendulum: balance is in, growth at all costs is out. Formerly backseat metrics like ARR/FTE, free cashflow (FCF) margin, R40 score, and gross dollar retention (GDR) come to the front seat joining net dollar retention (NDR) and ARR growth. ARR growth still predicts enterprise value (EV) multiples well -- but particularly if FCF margins are better than 15%. That means growth is great -- but only if you're profitable.

- The founder friendliness pendulum: the invisibility cloak loses some power. In the 2000s you'd routinely hear VCs whinging about "founder issues" at Buck's. But in 2009, with the founding of A16Z, came a new era of founder friendliness and along with it a founder invisibility cloak (or should I say invincibility cloak) whereby the presumption that the founder should run the company became nearly absolute. That pendulum will start to swing back in 2023.

- The employee friendliness pendulum. This is basic Michael Porter, but the new environment has reduced the bargaining power of employees. We'll discover that many of those perks and policies that were ostensibly rooted in culture and values were actually rooted in competition for labor. We're already hearing, "get back to the office" from Benioff et alia. Or unlimited PTO -- the ultimate perverse benefit -- from Microsoft. More companies will follow.

- The diligence pendulum: FOMO gives way to FOFU. In the past five years, I've never seen deals done faster in Silicon Valley, driven by a competitive market, growth investors with pre-conducted diligence, and a fear of missing out on investments. As the market cools, deals become less competitive, and stories like FTX emerge, things should return more to normal.

2. The barbarians at the gate are back. Valuations are down. Growth headwinds are up. S&M costs are high. Stock-based compensation (SBC) is increasingly controversial. That means activist investors will increasingly be swooping in to shake things up. And PE giants will increasingly be jumping in to clean things up. Anaplan and Zendesk were taken private in 2022. Salesforce is under pressure from two activist investors. Expect more of this activity to follow in 2023.

While it's not Henry Kravis at the gate this time, it's Robert Smith, Orlando Bravo, and Paul Singer. Management teams should prepare themselves for activist investors and adapt their financial profile to keep valuations high. While staggered boards and poison pills can stave off hostile takeovers, the best protection against an undesired acquisition is a high stock price.

- Retain is the new add. As companies prepare for a potential wave of churn, they put more emphasis on retention than ever before.

Why are companies afraid of churn in 2023?

- The downturn obviously puts cost pressure on customers. Must-have items can become nice-to-have overnight.

- SaaS sprawl. Per Statista, the average company uses over 100 SaaS apps and for many CFOs that's too many.

- SaaS rationalization. There's an entire emerging category of vendors (e.g., Cledara, Vendr, Vertice) who work to reduce SaaS spend. Their mission is to drive your churn.

- Consumption pricing. Consumption purists (without ratchets in their contracts) may well find themselves swimming naked as the tide goes out.

- Bankruptcy. Companies who sell to SMB may see increased amounts of uncontrollable churn as customers cease operations.

- Consolidation. Increased M&A can result in fewer, larger customers with larger discounts and lower costs per unit.

Companies increasingly have internalized the cost of churn. Namely that:

Cost to backfill churn = CAC ratio * churn ARR

That is, with a CAC ratio of 1.6, it costs $16M to backfill $10M in churn ARR.

While this bodes well for the customer success (CS) discipline, it does not automatically bode well for the customer success department.

Those business-oriented CS teams who thought customer advocacy meant generating customers who advocate for the company will continue to thrive. But those checklist-oriented CS teams who thought customer advocacy meant internal advocacy on behalf of customers may well find themselves restructured. With new cost pressure, the idea of funding an internal K Street is unattractive compared to redeploying those resources to the underlying engines of customer success, such as product, services, and support.

There are, after all, two sides to being in the spotlight.

- The Crux becomes strategy book of the year. Frequent readers already know that Good Strategy, Bad Strategy is my favorite book on corporate strategy. But my favorite part is how it eviscerates all the garbage that passes for strategy in corporate America.

In 2022, Rumelt published a second book, The Crux, which is more focused on how to build good strategy than on how to avoid bad strategy. I might have named the books Bad Strategy, Good Strategy and Good Strategy, Bad Strategy, respectively, but I suppose that would have been confusing.

I believe The Crux will become strategy book of the year in 2023 because:

- It takes a positive approach more than a critical one. Readers generally prefer that, and I think it's the one thing that held back Good Strategy, Bad Strategy.

- It frames strategy around the plan to overcome a critical strategic challenge. I believe 2023 will provide many companies with clear strategic challenges that need overcoming. Demand will be strong.

- He is logical, consistent, and practical in his thinking. Ruthlessly so. It's literally therapeutic to read Rumelt if you've spent enough years in the C-suite.

- Unlike business books that promise a magical answer (i.e., if you could just get <blank> right, then everything else will work), Rumelt offers a magical question: if you could just figure out the crux of your strategic challenge, then everything else can work.

The last point is not just verbal sleight of hand. Most business books preach a magical hammer (e.g., positioning, storybranding, category creation) -- learn to use this one tool and it will fix all of your problems. Rumelt does the opposite. He sets you on a search for the magical nail. Find that one problem -- that central knot or apparent paradox -- that, if overcome, will enable your success.

As he said in his first book, "a great deal of strategy work is trying to figure out what is going on. Not just deciding what to do, but the more fundamental problem of comprehending the situation." So true, yet so rarely admitted.

5. The professionals take over for Musk. While he's calmed down a fair bit since I wrote my original draft in December, I nevertheless believe that Elon Musk will hand over the CEO reins of Twitter in 2023. The announcement of his intentions isn't exactly news, but the question is will he actually do it? I think he will, largely because it won't continue to capture him the attention he needs and because the shareholders of Tesla will basically demand it.

I disclaim that I am not a Musk fanboy and that, in general, I am disappointed by the PayPal mafia, which I once saw as so full of promise. Perhaps my expectations were too high, but as both the Book of Luke and JFK have said, "to whom much is given, much will be required." Particularly, in Silicon Valley, where early success can launch a virtuous cycle of opportunity.

While Silicon Valley is a paragon of innovation, it most certainly is not a paragon of management. Musk exemplifies this: from improperly conducted layoffs to alienation of customers to product launch fiascos to total disrespect for product management and communications to CEO code reviews to self-contradictory policy statements to empty promises to dozens of other practices. Despite the thrill of working directly with the icon and megalomaniac, this simply isn't sustainable. The professionals will be tapped to take over in 2023.

- The bloom comes off the consumption pricing rose. Consumption pricing has been a hot topic for the past few years with many boards pressing companies to adopt consumption-based models. The conventional wisdom was roughly: if you want Snowflake's NRR of 160-180%, then you need to adopt their consumption-based model; you can't get there with per-seat annual SaaS or editions and upsells.

While consumption-based pricing tends to break SaaS metrics and while Snowflake is quick to explain that they are not a SaaS model, there has been significant pressure on enterprise software vendors to include at least a consumption-based component in their pricing. While this makes sense when passing along cloud-based infrastructure charges that scale with usage, when done in general, they forgot two things:

- To ask the customers. Wall Street loves 180% NRR, but what about Main Street? Do CFOs like when their software bill compounds upwards at an 80% rate? Methinks not.

- The tide also ebbs. During rising tides, users go up, usage goes up, and value delivered presumably also goes up. So maybe that 180% doesn't sting as much. But what about when these drivers go down? As Buffet said, only when the tide goes out do you see who's swimming naked.

In 2023, we'll see there are two types of consumption-based vendors: those with crafty CROs and those with purists. The crafties will have already structured ratcheted deals that can only go up year over year. The purists will not have built in that protection and will see consumption-driven churn as a result. By the end of 2023, we'll have many more crafty CROs and a lot fewer purists.

The early returns indicate that while consumption-based companies are seeing bigger hits to NRR, that they are nevertheless driving higher overall growth than their subscription-based counterparts.

Much like my PLG prediction last year, I don't think consumption-based pricing is dying. But I do think 2023 will remind everyone -- some via a slap in the face -- that there are two sides to the consumption-based coin.

- The rise of unified ops. The last decade has seen the rise of the "ops" function. Back when I was young, we didn't have ops. If you wanted reporting or analytics, you'd go to finance. But as functions become more automated, as each VP got their own app, and as CEOs and boards applied more pressure for quality reporting and analytics, each function got their ops person. Salesops, marketingops, supportops, servicesops, and successops. Sometimes these consolidated into revops or bizops. Often, however, they didn't.

What ensued was depressing. Siloed ops led to QBRs that resembled tag-team cagefights. When the CRO and the CMO were fighting, they'd tap in their respective ops heads to continue the brawl. My CXO versus your CXO. My ops person versus your ops person. My numbers versus your numbers. My model versus your model.

During an interim CMO gig, I worked with the CRO to unify the sales and marketing ops teams into a single revops team. Even though we were separate organizations both reporting to the CEO, we would have one unified ops team -- and we didn't care who it reported to. Attend both our staff meetings, but one set of numbers, one model, one forecast. What that gig ended, the first thing the new CMO did was disband it. Let the cage fights begin again. It's human nature.

That story notwithstanding, I think 2023 will see the rise of unified ops. Why?

- Cost pressures, and the need to increase efficiency. One single ops team, driving one set of modeling and reporting is cheaper to operate.

- CRO consolidation. As some customer success teams are integrated under the CRO, there will be a natural tendency to integrate salesops and successops.

- Model wars. CEOs get tired of having to say, "which model?" The saleops model? The FP&A model? The marketingops model? Why isn't there just one? There should be.

- Battle fatigue. Siloed ops isn't just inefficient, the conflicts it generates are highly visible. Over time, people get tired. A great ops leader should be an independent trusted advisor to the business, not a personal pit bull in each CXO's corner.

- Resource flexibility. A single team can move resources dynamically to meet the challenges at hand.

- Software standardization. Rationalizing SaaS costs and eliminating stack redundancy is easier when the various ops functions are in a single team.

- End-to-end funnel analysis. Breakpoints in the funnel cause problems -- e.g., sales doesn't just want 500 oppties generated this quarter, they want the good ones. But which are the good ones? The ones that close. But which are the good ones for success? The ones that renew and expand. How can we generate those? One team, looking end to end, is in the best position to do this analysis.

For all these reasons, I believe (and hope) that 2023 will see the rise of unified ops.

8. Data notebooks as the data app platform. I'll preface this by saying I'm an angel investor in Hex, who raised a $52M round from A16Z last year, so I'm excited about data notebooks for more than one reason.

While data notebooks are old hat to most data scientists, for business analysts and business users, they are still relatively unknown. Descended from Jupyter notebooks, today's data notebooks (e.g., Hex, Notable) generally position as something larger, platforms for collaborative analytics and data science.

When it comes to Jupyter notebooks, this tweet was my introduction to the subject, which got me reading the underlying notebook by Kevin Systrom.

The highest quality Jupyter notebook I've ever seen was just posted by... <checks notes>... ex-CEO of Instagram, Kevin Systrom?

h/t (@seanjtaylor )https://t.co/LU1PSHNveW

— Chris Said (@Chris_Said) April 13, 2020

Systrom's notebook is basically a research paper, built in collaboration, with equations; embedded, executable code; its outputs; configuration management; dependency graphs; and more. Compare that to the unmanaged spreadsheets you probably use to run your business today.

So the idea of generalizing this to data problems and data users of all types was instantly appealing to me. I remember when I first met with Barry at Specialty's, he framed the problem as wrapping models. As data scientists, we can build models, but we need to wrap them in apps -- what we'd now call data apps -- so users can use them. Much as a spreadsheet has a builder and a user (think: lock down all the cells but a few inputs), a more sophisticated model can and needs to be wrapped as well. But wrapping a model means effectively building an application, and with that comes a dreaded backlog for building and maintaining those applications. It was a flashback to enterprise reporting circa 2000 (back when you had the report backlog) and I was instantly hooked.

While I'm not sure I agree with Martin Casado that all SaaS apps will be remade as data apps, I do believe the world is ready for data apps. I see them, perhaps in a more pedestrian fashion, as these integrated notebooks of code (including not only Python but SQL), no code alternatives, sequencing, models, narrative, metadata, and collaboration -- and wrapped and ready for consumption. That's why I'm a big believer in data apps and I see data notebooks as the platform for building the first generation of them. Check out the Hex demo on their home page for a five-minute look.

9. Meetings somehow survive. To paraphrase Twain, reports of the death of meetings have been greatly exaggerated. While I'll confess to the imprudence of giving Death By Meeting to my boss shortly after its publication, the death of meetings is an entirely different matter. In January, Shopify announced what appeared to be a total meeting ban, but in reality was a ban on scheduled recurring meetings with three or more people along with a two-week cooling-off period before meetings could be added back to calendars. Nevertheless, this resulted in the cancellation of 10,000 meetings.

While the move provoked some debate, some backlash, and some discussion of DEI implications, it also provoked some pile-on, often under the fairly offensive slogan, "companies are for builders, not managers."

The death to meetings crowd makes a number of mistakes in its thinking:

- That everyone is engaged in individual work, like coding or writing. How should, e.g., an HR business partner add value by not meeting with people? Or an BDR manager?

- That managers somehow do not contribute to building a company. Great, let's get 100 developers all reporting to the CEO and see what happens.

- That all meetings are bad. There's a clear baby/bathwater issue here.

- That online alternatives can replace meetings. The limitations of email and Slack are well known. They're great for some things and rotten for others. My personal rule: never try to resolve a hard issue over either.

- That cadence is unimportant. I believe that the cadence of regular meetings says a lot about a company -- e.g., a weekly vs. a monthly forecast call, or a monthly vs. quarterly sales close.

- That meetings cannot be improved. In reality, the goal with meetings, as with any tool, is to use them when appropriate. The quest is to focus on making them better. I say quest because to do so is both difficult and endless: as this article from 1976 demonstrates.

10. Silicon Valley thrives again in 2024. While I believe 2023 will be a tough, character-building year for startups, we must remember that this is simply another cycle of creation and destruction in Silicon Valley. The bad news is that companies will be increasingly faced with difficult, sometimes existential, decisions. The good news for me (at least) is that demand for gray hair seems to go up when the markets go down. The good news for everyone is that this is simply a cycle, one from which we shall emerge, and when we do so, the world we emerge into will be more rational and fundamentals-focused.

Until then, stiff upper lip, hunker down, and buckle up.

Virgil

# # #

Notes

[1] I inadvertently published an incomplete version of this post on 2/1/23 around mid-day. While I instantly removed it from the blog, LinkedIn, and Twitter, I was unable to recall the post sent to email subscribers. Please accept my apologies for this mistake. While there are a few tricks one can use to avoid such problems (e.g., publish later, don't create in the Wordpress editor), I was on approximately draft 67 of this post, meaning that 66 times I correctly hit "save draft," but alas once hit "publish" and off it went.