You've Been Asked To Be a Startup Advisor: Now What?

“You’re fired,” said the general counsel (GC) of the public, multi-billion-dollar software company and I wasn't just happy, I was ecstatic.

I’d known this company for a long time. I’d helped their VCs with diligence. I’d worked with them in the early days as an advisor, and received a stock option as compensation. So when I contacted the company to sell the shares (from the option I’d exercised long ago), I was surprised to find a folder called “Grant 2." They’d given me a second grant that I'd actually forgotten about. OMG, this was my lucky day.

I told the stock administrator that I wanted to exercise the second option grant.

“You can’t,” she said. “It’s been canceled.”

“Why?” I said, watching a G-Wagon disappear before my eyes.

“Because you discontinued your service to the company.”

“No, I didn’t. You just stopped calling. That’s the nature of advisory work. You call and I answer.”

This launched a multi-week argument about if and when I’d stopped providing services and many questions about why I’d not been notified of any termination -- so I’d have at least known the 90-day option exercise window had started. The dispute eventually escalated to the GC who, in firing me, started my 90-day clock, admitting the option was still valid.

Why do I tell you this story? First, because it’s hilarious. The GC could easily just have said he’d honor the option, but instead chose to communicate that good news by firing me. Second, because this is what happens when you use paperwork written for employees to engage with advisors.

In this post, I’ll share what I’ve learned over the past fifteen years advising startups to give you a better idea of what to do when someone asks you to advise their startup. See my disclaimers, remember that this is not legal or financial advice and that you should hire professionals to get advice specific to your situation.

When asked to be an advisor of an early-stage company, I think you should do four things:

- Decide if you want to advise the company

- Discuss and set clear expectations on both sides

- Agree on compensation, which is typically but not always, stock

- Put a good, quick legal agreement in place

Decide If You Want to Advise the Company

This may seem like an obvious first step, but sometimes the answer really should be no. There are lots of good reasons to advise a company. For example, you can:

- Build your network with the company’s team and investors

- Learn by seeing more business situations

- Sow seeds for potential downstream relationships (e.g., employee or board)

- Pay it forward

But there are also some good reasons not to advise a company, including:

- Bad chemistry. Life’s too short. Avoid deals where the investors are trying to impose you as an advisor to a reluctant executive.

- Poor fit. You want to be asked about problems you’ve seen dozens of times. You’ll give better answers and it will take less of your time.

- When they have a one-shot problem. Advising is a long-term, relationship game. If a company just needs help with one thing (e.g., positioning, re-organization), everyone could be better off if you do a cash consulting deal or just offer some input for free.

- Restrictive terms in the advisor agreement, such as non-solicitation, no-hire, or non-compete agreements. Once you’re advising company A, you may discover that you wish you were advising company B. While switching horses may or may not be prohibited under the agreement, it’s always bad form and bad for your reputation. This is now the top reason I decline advisory deals. There is an opportunity cost associated with advising that many overlook.

Discuss and Agree on Clear Expectations

I don’t think this needs to be contractual -- or even necessarily written down since most agreements feature bilateral termination for convenience anyway -- but I do think it’s important to have a detailed conversation about expectations.

These are all great topics to include in that conversation:

- The specific areas where the company wants help. For me, that might be SaaS metrics, marketing, board presentations, and CEO mentoring.

- The form of the help. Some people want you to build their financial model; I just want to provide feedback to your finance head who can then iterate and improve it themself.

- Interaction frequency. For me, that’s typically measured in times per month.

- In-office attendance. Some of my friends like to show up once/week and have watercooler encounters to really get to know the company and its scuttlebutt. Me, not so much.

- Periodic vs. ad hoc meetings. I like to meet because there’s something to discuss, not because it’s Tuesday. But different people see this differently and compensation structure impacts this as well.

- Time commitment. Some people like to agree on hours/month, I don’t. When you buy experience, you're paying for fast answers, so hours is the wrong metric. Value is measured by how quickly I can solve a problem, not how slowly.

Agree on Compensation

Because I’m talking about early-stage (e.g., seed, pre-seed) advisory, the typical company doesn’t have much cash and wants to pay advisors in stock, typically measured in the tenths of a percent.

Let's do some sample math which will rely on a bunch of assumptions:

- Shares granted: 0.2%

- Anticipated dilution before exit: 50%

- Shares after dilution: 0.1%

- Assumed exit price: $500M

- Value: $500K

- Probability: 5%

- Expected value: $25K

- Hours invested over 7 years at 2 hours/month: 168 hours

- Expected value, hourly rate: $149

You might see the $500K here and think “amazing money,” and you’d be right -- in the unlikely case this actually happens. In a more realistic $500M exit scenario, those shares might be worth $250K due to debt and preferences. In a dire scenario, e.g., with multiple liquidation preferences and a large amount of capital raised, they might be worth $0.

(Note that this example assumes no debt, no participating preferred shares, and an exit value that clears the preference stack by enough that all investors take their pro rata ownership instead of their preferences.)

So, to go back to the point – the majority of these deals pay $0 to the advisor. When you average out the occasional big hit across the rest you might end up making $150/hour. And the cashflow is lumpy. It's a fun hobby, but it's no way to make a living.

So, when evaluating an advisory opportunity, do the math and run some scenarios. Then think about the commitment you’re willing to make. And, more than anything, do the work because it’s fun and you grow by doing it -- not because you’re banking on any big hit.

If you consider any compensation whatsoever as upside, you’ll always be happy -- and maybe sometimes when you get lucky -- very happy.

Put a Good, Quick Legal Agreement in Place

The problem here is that neither side is interested in spending money on a good advisor agreement. The cash-starved startup, running on the founder's savings, doesn't want to. Nor does the would-be advisor, who's well aware their most likely outcome is $0. Who wants to spend a few thousand in legal fees on that?

So you end up running on a stock-option agreement written for employees that you repurpose for advisors (which was the case with my company in the opening story). Or a consulting agreement. Or a simple letter. Or nothing at all.

None of that sounds very good to me.

What do I do in this situation? I start with the FAST advisory agreement. I like it because:

- It’s standard. To my knowledge a lot of people use it.

- It’s neutral, not having been created by either the company or the advisor.

- It covers many of the obvious basics (e.g., non-disclosure, independent contractor relationship, non-conflict).

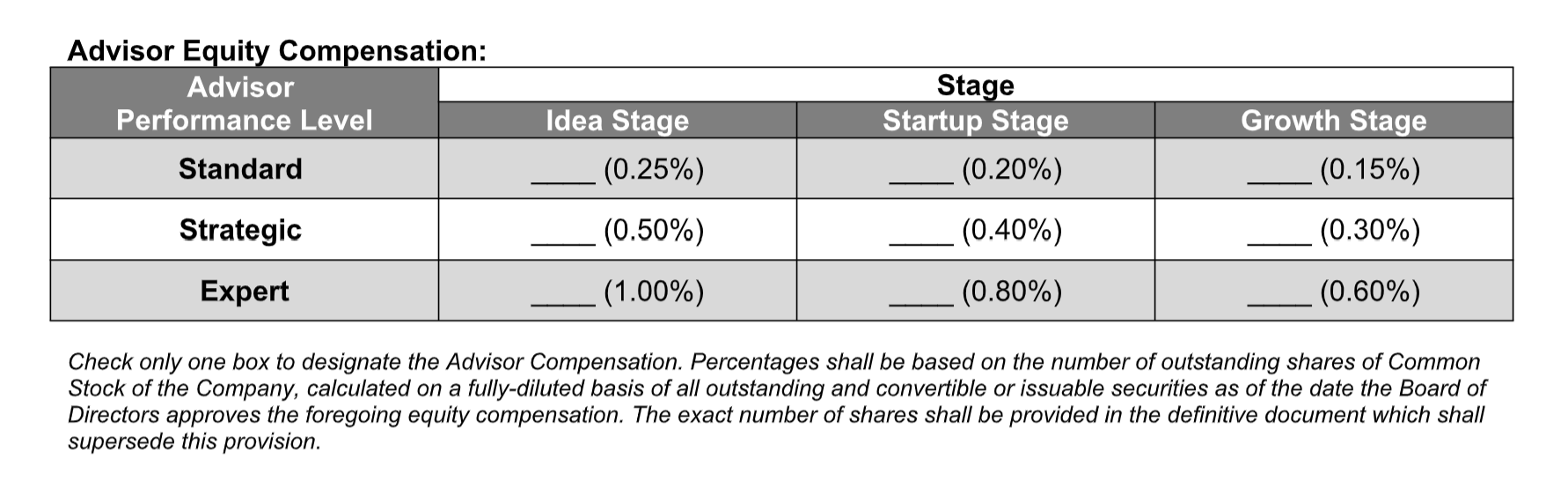

- And, if you want to use their matrix, it even includes compensation.

I'm not a lawyer (and you should ask your own), but the FAST agreement strikes me as doing a reasonable job of providing a stage-appropriate agreement for advising an early-stage company. Per the Founder Institute who's created it:

The FAST Agreement is used by tens of thousands of entrepreneurs and advisors per year to establish productive working relationships, trading advice and support for a standardized amount of equity. [...]

With just a signature and a checkbox on the FAST Agreement, entrepreneurs and advisors can agree in minutes on how to work together, on what to accomplish, and on the right amount of equity compensation.

The only catch is that while I like the compensation matrix and the idea of using stage vs. expertise to determine compensation, I don’t like the specific definitions in Schedule A because, among other reasons, they include fixed time commitments that I think are too high. So I either negotiate them out or rewrite that schedule.

I hope this post will help you in thinking about your next steps when and if someone asks you to advise their startup.