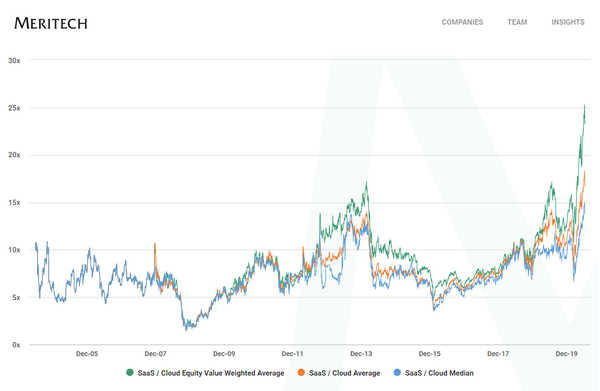

Finance

"All Models Are Wrong, Some Are Useful."

"I have a map of the United States ... actual size. It says, Scale: 1 mile = 1 mile. I spent last summer folding it. I also have a full-size map of the world. I hardly ever unroll it." -- Stephen Wright (comedian) Much as we build maps as models