Back in 2018, Rory O’Driscoll, a VC at Scale and the inventor of the SaaS magic number, came up with another important SaaS concept: the Mendoza line for SaaS growth. Taking an idea from baseball, the Mendoza line is a measure of “offensive futility” named after Mario Mendoza, one of the best defensive shortstops in baseball, who unfortunately was challenged as a hitter, constantly struggling to maintain a .200 batting average. The question considered by the Mendoza line is: how low a batting average can a player have and remain in Major League Baseball, even with a very high level of defensive talent? The answer, in Mendoza’s day, was around .200. Above that, they’d keep you on the team for your defensive abilities; below that, they’d probably send you down to the minor leagues [1].

Driscoll translated this concept to SaaS, creating a line that provides, across a range of ARR sizes, a growth rate below which a company is not on a venture-backable trajectory. In short, if you’re above the SaaS Mendoza line, VCs will want to invest in your company, and if you’re not, they won’t. So it’s an important concept and one that helps answer a very difficult question for founders: how fast should we be growing?

Here’s the Mendoza line from Rory’s original post:

Note that the Mendoza line is a growth trajectory rule and thus should be considered along with other growth trajectory rules and metrics like T2D3 (triple, triple, double, double, double) by Battery’s Neeraj Agrawal, the growth endurance observations periodically discussed by Janelle Teng of Bessemer, or my Rule of 56789 published with my then-colleague at Balderton, Michael Lavner.

The inspiration for today’s post was a recent update to the SaaS Mendoza line published by Scale’s Eduard Danalache in July. Since the line changed with this update, I’ll refer to the original as the 2018 Mendoza line and the new one as the 2024 Mendoza line.

Now, let’s dive in.

The Two Assertions Behind the 2018 Mendoza Line

O’Driscoll said the Mendoza line was based on two assertions (paraphrased):

- That most venture investors prefer to invest in companies with a chance to become standalone public companies. Looking at the (then-)realistic low bar of what that takes, this implied ARR of $100MM at the time of IPO, while still growing at 25% or greater.

- That, most of the time, growth rates decline in a way that is fairly predictable. For a best-in-class SaaS company, the growth rate for any given year is between 80% and 85% of the growth rate of the prior year. Scale refers to this as growth persistence and argues this assumption holds true from about $10M on.

Some quick comments:

- My how times have changed. Last week, I heard OneStream, at nearly $500M in ARR, referred to as “on the small side” for an IPO today [2]. That’s five times bigger than Rory’s bar, set only six years ago. Since a viable path to IPO is inherent in the definition of the SaaS Mendoza Line, the math needs to be updated to account for this.

- What Scales calls “growth persistence” is now commonly called growth endurance. I’ll use the latter term henceforth.

There were some objections to the Mendoza line when it was introduced and Scale responded to them with a follow-up post. It’s a good read, but I won’t dig into it here. The headline news is simple: somebody needs to update the math.

The 2024 Mendoza Line

Last month, Scale released an update entitled, The Path From Zero to IPO: Revisiting the Mendoza Line in 2024.

The first thing they did was change the IPO criteria:

For the sake of this analysis, we’ll use a more ambitious target of $250M ARR growing at 25%, with a clear path to profitability. Again, don’t take this as gospel truth for when to IPO, but for the math to work we have to draw a line in the sand to aim for, and we believe this is a fair target in today’s world.

While this raises the bar significantly, I think it’s still too low. Anecdotally, per some recent Meritech S-1 breakdowns:

- OneStream just went public with ARR of $480M growing at 34%

- Rubrik went public earlier this year with $784M of ARR, growing at 47%

- Klavyio went public in 2023 with $658M of implied ARR, growing at 51%

The last Meritech breakdown that resembles their target is Hashicorp, which went public in 2021 with $294M of ARR but was growing at 50%. But that stock, after some initial highs, was basically a dud in the public markets, so it’s perhaps not the ideal case study.

If I had to guess, I’d say the IPO bar today for software companies is more like $400M growing at 40% than $250M growing at 25% [3]. Many, me among them, would argue that the bar is much higher than it needs to be, but there are things we can’t control and this is certainly one of them.

Once you pick the destination (in terms of size and growth rate) and the growth endurance factor (Scale picks 85%), the rest is just a math problem.

But with one catch. Where do you start? The 2018 Mendoza line chart goes all the way down to $1M in ARR [4]. In the 2024 version, they basically say we don’t care how you get to $10M, but once you get there the Mendoza line takes effect.

Here’s the chart they published that compares the 2018 and 2024 Mendoza lines.

And here’s me backing into a curve based on the targets for ending ARR, growth rate, and growth endurance [5].

Running this model forward is all just about powers of 0.85. You pick a starting size, growth rate, and GE factor. You then use the GE factor (85%) to shrink the growth rate every year. So, for example, after 3 years your growth rate 0.85^3 = 61% of what it started at.

The problem with powers of 0.85 is they don’t scale very well. Scale realized this in scaling down, hence the 2024 advice to apply the rule only at $10M+. But, by picking the $250M ending target, they also avoided a degree of scaling up, pushing the rule to the edge of where it stops working because after about 10 years the growth rates it produces are too low. For example, the year 11 the growth rate is only one-fifth of what it was at the “start” [6].

So I’d say the 2024 Mendoza line is decent, but it doesn’t scale infinitely and is best used within a range, starting at $10M and for about the next 10 years.

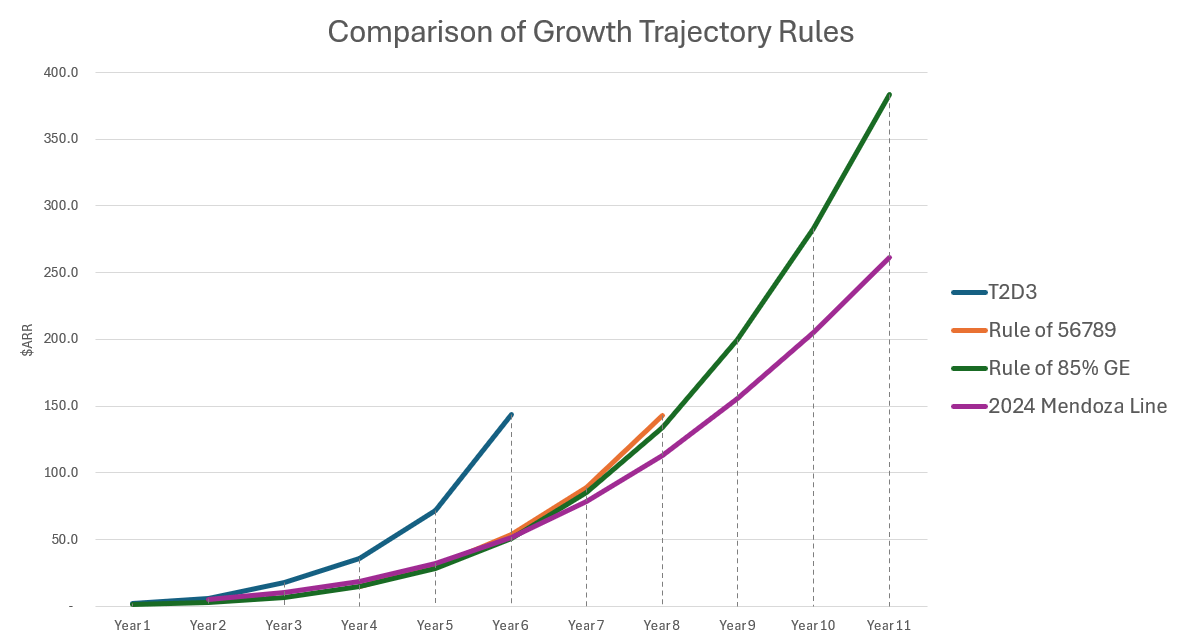

Comparison to Other Growth Trajectory Rules and Metrics

Let’s conclude by comparing the Mendoza line to other rules and metrics for thinking about startup growth trajectory. Namely:

- T2D3, which says once a company hits $2M in ARR it should seek to triple twice and then double three times.

- The Rule of 56789, which says that startups should seek to break $10M in 5 years, $20M in 6 years, $50M in 7 years, $75M in 8 years, and $100M in 9 years [7].

- The 85% growth endurance rule, which says you should pass $1M at some very high growth rate, then retain 85% of that growth every subsequent year [8]. I only now realize this is essentially a Mendoza line rose by any other name — which highlights a disadvantage of using catchy names (e.g., magic number, Mendoza line) over descriptive ones [9].

Here’s a tabular comparison of these rules [10]:

The outlier is T2D3 which I suspect has some lingering ZIRP growth-at-all-costs logic built in. The other rules tend to generate similar trajectories, none of which (by the way) get you to an IPO in 12 years. This is consistent with what I’m guessing is today’s median of around 14 years to IPO. More than ever, building a startup from inception to IPO is a marathon, not a sprint. Spend your energy accordingly.

Finally, for those who prefer charts, here is a visual comparison of those trajectories.

In this post, we’ve examined the 2024 Mendoza line for SaaS and learned a few things in the process:

- That the 2018 Mendoza line is hopelessly out of date given the market changes in IPO requirements. This might explain why it never became as popular as other Scale creations like the magic number.

- That since top VCs want to invest in companies that have a shot of going public, that founders should keep an eye on growth trajectories and the outcomes to which they lead. Specifically, if you’re clearly on a trajectory that cannot lead to an IPO, maybe should raise money through PE, regional and/or lower-tier VCs with lesser ambitions, venture debt, or revenue-based financing.

- That the Mendoza line is a fancy way of saying retain 85% of your growth each year and (in the 2024 version) that you should start applying it after $10M. Personally, I’ll just use the 85% growth endurance rule as I think it’s simpler and comes without the somewhat arbitrary provisos.

- That these rules only work within certain zones. T2D3 works from $2M to $144M and is undefined after that. The 2024 Mendoza line works from $10M to $250M, but beyond that produces growth figures that are too low. The 85% growth endurance rule works across the broadest range, but relies on starting at small size with an amazing growth rate from which to decay.

- That rules reflect the environment in which they were created. The 2018 Mendoza line took you to $100M, which was Scale’s assumed IPO bar in 2018 [11]. T2D3 has an in-built high-growth bias reflective of the ZIRP era and best applied today only in greenfield markets where you have lots of capital available (e.g., AI).

- That God did not decree that growth needs to decay every year. While this is certainly a common pattern, I have run startups where we accelerated growth (i.e., GE of >100%) and the average growth rate in Meritech’s public comparables is 19% today, higher than the age-driven growth rates which the Mendoza line would imply [12].

Thanks for reading. The spreadsheet I used in making this post is here.

# # #

Notes

[1] Fans will be happy to know that Mendoza ended his career with a .215 batting average. The lowest hitting shortstop today is batting .219.

[2] To really blow your mind, back at Business Objects, we went public in 1994 off $30M in revenues, which was fairly normal at the time. The IPO bar has gone way, way up over the decades and changed many things in Silicon Valley as a result. For example, creating the entire asset class of VC/PE growth equity which was unnecessary when companies went public with a $100M round off $30M in revenues.

[3] The IPO bar is ever-changing, somewhat ill-defined, and not something you can easily get data on unless you’re friendly with a bunch of investment bankers. For more data, go here, here, and here.

[4] Which is odd because the text of the article says the growth endurance behavior doesn’t start until $10M. I suspect the comment was added after the initial posting and the spreadsheets weren’t changed.

[5] Note that Mendoza line is presented as a curve which makes me think they calculated the equation for this curve and then plugged in the nice neat 10, 20, 30, etc. ARR sizes along the bottom. See my spreadsheet where I do that using an Excel trendline and accompanying formula.

[6] That is, your growth rate in the year in which you passed $10M.

[7] Reminder: this is about a trajectory and break means break, not hit. Some people misread the rule by translating the thresholds to growth rates which is not correct. By the way, those figures were arrived at by seeing what it took to be top quartile in the Balderton universe of data.

[8] I called it Growth Retention Rule in the 56789 blog post but don’t like how that abbreviates to GRR, so I switched to Growth Endurance here both to use today’s more commonplace language and avoid ambiguity around GRR (which means gross retention rate to most).

[9] It maps pretty well to the 2018 Mendoza line, though today’s now starts at $10M per Scale.

[10] Where the second and third rows are not the only possible trajectories, but each an example of a reasonable rule-compliant trajectory.

[11] I still think that was a low-ball estimate even in 2018.

[12] Though, in defense of Scale, they argue the Mendoza line is a tool for determining if you’re on an IPO trajectory and it was not designed to work beyond the IPO timeframe.

Hey Dave! In your Rule of 85% GE example, what were reasons for starting at $3m in year 3 / growth rate of 153%? I may have missed it.

Perhaps I was too subtle. I used those numbers because there were the ones I (arbitrarily) picked in The Rule of 56789 post. The main point being that if you start small enough with a high enough growth rate, you actually run with steady 85% decay for a long time. But short answer is they were arbitary but consistent with the ones I showed in the other post.

Okay great. Thanks!