The Rule of 40 -- Down, But Not Out!

Neeraj Agrawal and Logan Bartlett of Battery Ventures recently published the 2019 version of its outstanding annual software round-up report. I highly recommend this report -- it's 78-pages chock full of great data about topics like:

- Why Battery is long software overall

- The four eras of software evolution

- The five forces driving software's accelerating growth

- Key trends in 2018, including setting records in three areas: (1) public company revenue multiples, (2) IPO volume (by over 2x), and (3) M&A volume (by over 2x).

- Key trends from their 2017 report that are still alive, well, and driving software businesses.

But, most of all, it has some great charts on the Rule of 40 [1] that I want to present and discuss here. Before doing that, I must note that I drank today's morning coffee reading Alex Clayton's CloudStrike IPO breakdown, a great post about a cloud security company with absolutely stunning growth at scale -- 121% growth to $312M in Ending ARR in FY19. And, despite my headline, well in compliance with the Rule of 40. 110% revenue growth + -26% free cashflow margin = 84%, one of the highest Rule of 40 scores that I've ever seen [2]. Keep an eye on this company, I expect it should have a strong IPO [3].

However, finding one superstar neither proves nor disproves the rule. Let's turn to the Battery data to do that.

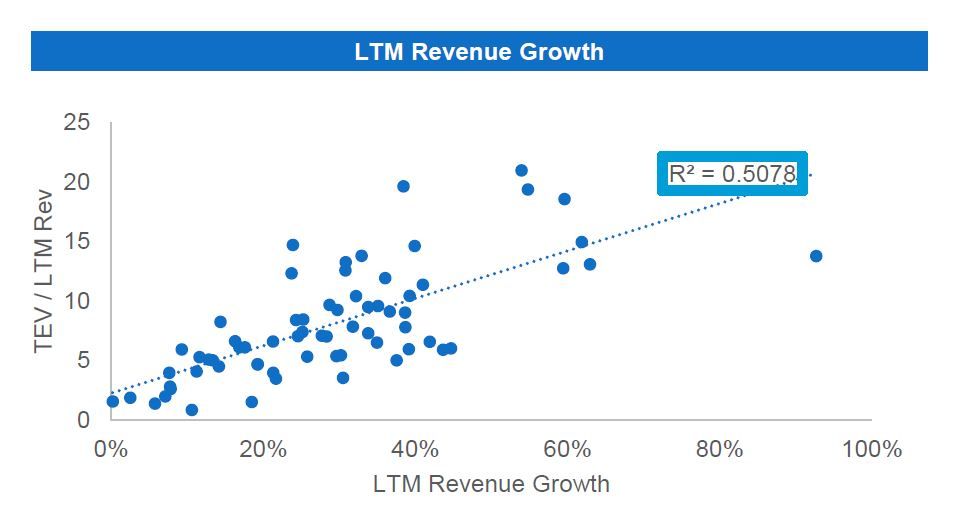

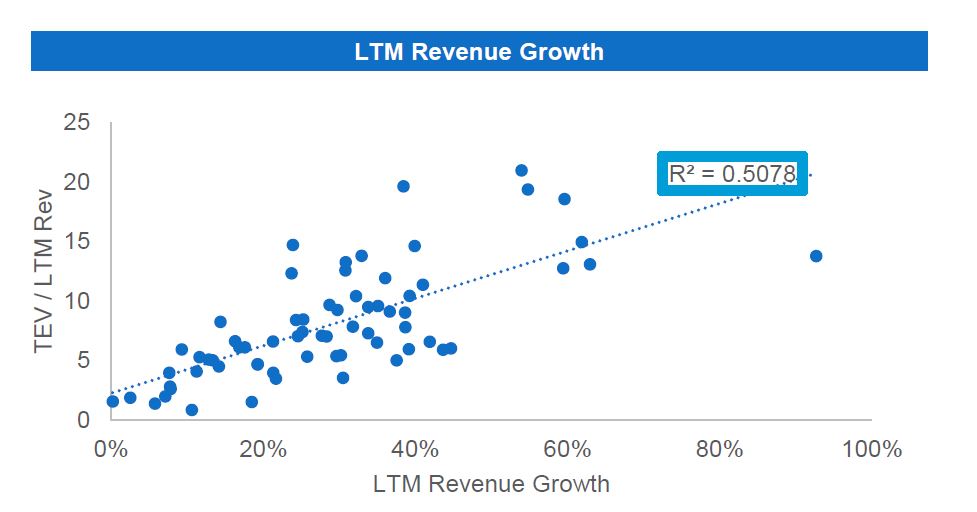

When discussing the Rule of 40, most financial analysts make one of two plots.

- They do a scatter plot with revenue growth on the X-axis and FCF margin on the Y-axis. The Rule of 40 then becomes a line that separates the chart into two zones (compliant and non-compliant). Note that a minority of public companies actually comply suggesting the rule of 40 is a pretty high bar [4].

- Or, more interestingly, they do a linear regression of Rule of 40 score vs. enterprise-value/revenue (EV) multiple. This puts focus on the question: what's the relationship between Rule of 40 score and company value? [5]

But that thing has always bugged me is that nobody does the linear regression against both the Rule of 40 score and revenue growth. Nobody, until Battery. Here's what it shows.

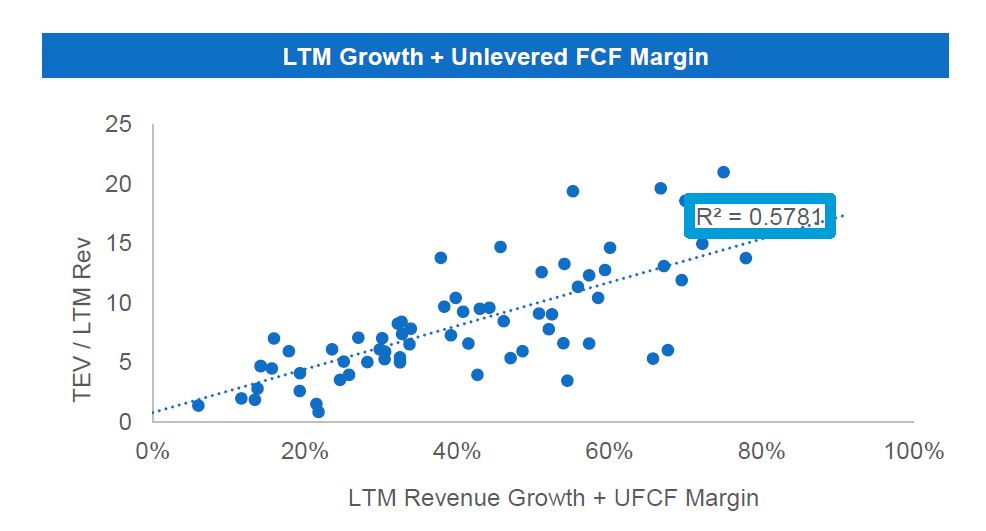

First, let's look at the classic Rule of 40 regression. Recall that R-squared is a statistical measure that explains the dependence of the dependent variable (in this case, EV multiple) on the independent variable (Rule of 40 score). Here you can see that about 58% of the variation in enterprise value multiple is explained by Rule of 40 score. You can intuit that by looking at the dots relative to the line -- while there is clearly some linear correlation between the data, it's a long way from perfect (i.e., lots of dots are pretty far from the line). [6]

Now, the fun part. Let's see the same regression against revenue growth alone. R-squared here is 51%. So the explanatory power of the Rule of 40 is only 7% higher than revenue growth alone. Probably still worth looking at, but it sure gets a lot of PR for explaining only an incremental 7%. It could be worse, I suppose. Rule of 40 could have a lower R-squared than revenue growth alone -- in fact, it did back in 2008 and in 2012.

In the vein, for some real fun let's look at how this relationship has changed over time. The first thing you'll notice is that pre-2012 both last twelve month (LTM) revenue growth and the Rule of 40 had far weaker explanatory power, I suspect because profitability played a more important role in the equation. In 2012, the explanatory power of both metrics doubled. In 2015 and 2016 the Rule of 40 explained nearly 20% more than revenue growth alone. In 2017 and 2018, however, that's dropped to 7 to 8%.

I still think the Rule of 40 is a nice way to think about balancing growth vs. profit and Rule of 40 compliant companies still command a disproportionate share of market value. But remember, its explanatory power has dropped in recent years and, if you're running an early or mid-stage startup, there is very little comparative data available on the Rule of 40 scores of today's giants when they were at early- or mid-stage scale. That's why I think early- and mid-stage startups need to think about the Rule of 40 in terms of glideslope planning.

Thanks to the folks at Battery for producing and sharing this great report. [7]

# # #

Notes[1] Rule of 40 score = typically calculated as revenue growth + free cashflow (FCF) margin. When FCF margin is not available, I typically use operating margin. Using GAAP operating margin here would result in 110% + -55% = 55%, much lower, but still in rule of 40 compliance.

[2] If calculated using subscription revenue growth, it's 137% + -26% = 111%, even more amazing. One thing I don't like about the fluidity of Rule of 40 calculations, as you can see here, is that depending what might seem small nuances in calculations, you can produce a very broad range of scores. Here, from 55% to 137%.

[3] To me, this means ending day 1 with a strong valuation. The degree to which that is up or down from the opening price is really about how the bankers priced the offer. I am not a financial analyst and do not make buy or sell recommendations. See my disclaimers, here.

[4] In fact, it's actually a double bar -- first you need to have been successful enough to go public, and second you need to clear the Rule of 40. Despite a minority of public companies actually clearing this bar, financial analysts are quick to point out the minority who do command a disproportionate share of market cap.

[5] And via the resultant R-squared score, to what extent does the Rule of 40 score explain (or drive) the EV/R multiple?

[6] If R-squared were 1.0 all the dots would fall on the least-squares fit line.

[7] Which continues with further analysis, breaking the Rule of 40 into 4 zones.