An Update on the SaaS Rule of 40

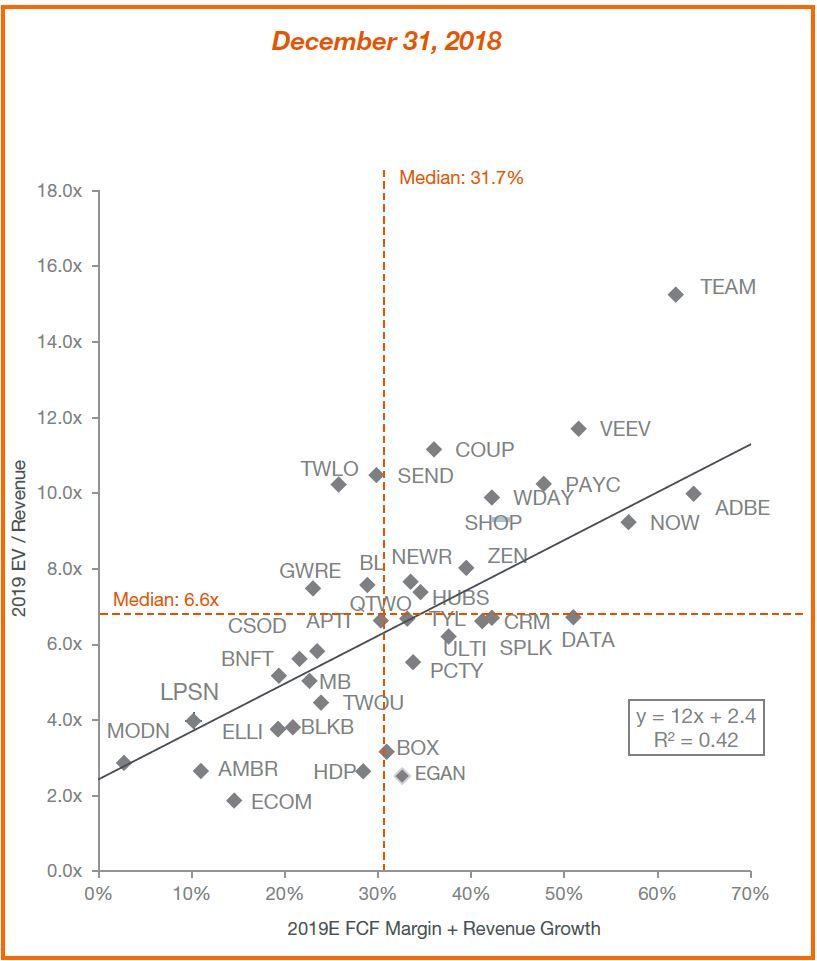

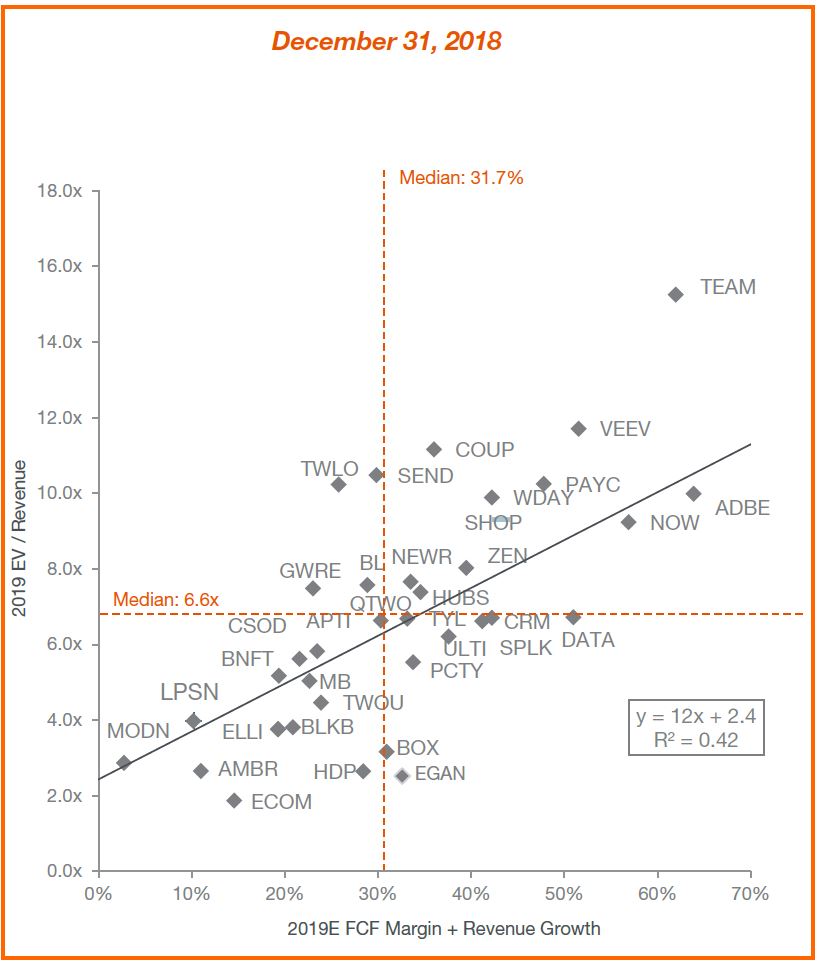

Thanks to the folks at Piper Jaffray and their recently published 2018 Software Market Review, we can take a look at a recent chart that plots public software company enterprise value (EV) vs. Rule of 40 (R40) score = free cash-flow margin + revenue growth rate.

As a reminder, the Rule of 40 is an industry rule of thumb that says a high-growth SaaS company can burn as much cash as it likes in order to drive growth -- as long as its growth rate is 40 percentage points higher than its free cashflow margin. It’s an attempt at devising a simple rule to help software companies with the complex question of how to balance growth and profitability.

One past study showed that while Rule of 40 compliant software companies made up a little more than half of all public software companies that they captured more than 80% of all public market cap.

Let’s take a look at Piper’s chart which plots R40 score on the X axis and enterprise value (EV) divided by revenue on the Y axis. It also plots a presumably least squares fit line through the data points.

Source: PJC Analysis and SAP Capital IQ as of 12/31/2018

Of note:

- Less than half of all companies in this set are Rule of 40 compliant; the median R40 score was 31.7%.

- The median multiple for companies in the set was 6.6x.

- The slope of the line is 12, meaning that for each 10 percentage points of R40 score improvement, a company's revenue multiple increases by 1.2x.

- R^2 is 0.42 which, if I recall correctly, means that the R40 score explains 42% of the variability of the data. So, while there's lots it doesn't explain, it's still a useful indicator.

A few nerdier things of note:

- Remember that the line is only valid in the data range presented; since no companies had a negative R40 score, it would be invalid extrapolation to simply continue the line down and to the left.

- Early-stage startup executives often misapply these charts forgetting the selection bias within them. Every company on the chart did well enough at some point in terms of size and growth to become a public SaaS company. Just because LivePerson (LPSN) has a 4x multiple with an R40 score of 10% doesn’t mean your $20M startup with the sames score is also worth 4x. LPSN is a much bigger company (roughly $250M) and and already cleared many hurdles to get there.

The big question around the Rule of 40 is: when should companies start to target it? A superstar like Elastic had 76% growth and 8% FCF margin so a R40 score of 84% at its spectacular IPO. However, Avalara had 26% growth and -28% FCF margin for an R40 score of -2% and its IPO went fine. Ditto Anaplan.

I'll be doing some work in the next few months to try and get better data on R40 trajectory into an IPO. My instinct at this point is that many companies target R40 compliance too early, sacrifice growth in the process, and hurt their valuations because they fail to deliver high growth and don't get the assumed customer acquisition cost efficiencies built in the financial models, which end up, as one friend called them, spreadsheet-induced hallucinations.