Financial analysts speak a lot about “billings” in a public SaaS companies, but in private VC-backed SaaS companies, you rarely hear discussion of this metric. In this post, we’ll use a model of a private SaaS company (where we know all the internal metrics), to show how financial analysts use rules of thumb to estimate and/or impute internal SaaS metrics using external ones – and to see what can go wrong in that process.

For reference, here’s an example of sell-side financial analyst research on a public SaaS company that talks about billings [1].

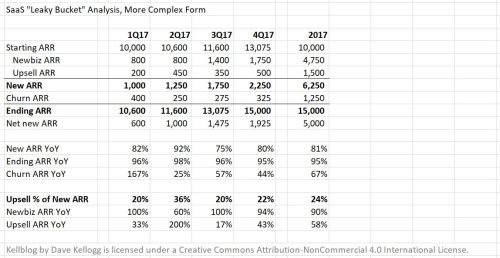

Let’s start with a quick model that builds up a SaaS company from scratch [1]. To simplify the model we assume all deals (both new and renewal) are for one year only and are booked on the last day of the quarter (so zero revenue is ever recognized in-quarter from a deal). This also means next-quarter’s revenue is this-quarter’s ending annual recurring revenue (ARR) divided by 4.

Available to renew (ATR) is total subscription bookings (new and renewal) from four quarters prior. Renewal bookings are ATR * (1 – churn rate). The trickiest part of this model is the deferred revenue (DR) waterfall where we need to remember that the total deferred revenue balance is the sum of DR leftover from the current and the prior three quarters.

If you’re not convinced the model is working and/or want to play with it, you can download it, then see how things work by setting some drivers to boundary conditions (e.g., churn to 0%, QoQ sales growth to 0, or setting starting ARR to some fixed number [2]).

The Fun Part: Imputing Internal Metrics from External Ones

Now that we know what’s going on the inside, let’s look in from the outside [3]:

- All public SaaS companies release subscription revenues [4]

- All public SaaS companies release deferred revenues (i.e., on the balance sheet)

- Few SaaS companies directly release ARR

- Few SaaS companies release ATR churn rates, favoring cohort retention rates where upsell both masks and typically exceeds churn [5]

It wasn’t that long ago when a key reason for moving towards the SaaS business model was that SaaS smoothed revenues relative to the all-up-front, lumpy on-premises model. If we could smooth out some of that volatility then we could present better software companies to Wall Street. So the industry did [6], and the result? Wall Street immediately sought a way to look through the smoothing and see what’s really going on in the inherently lumpy, backloaded world of enterprise software sales.

Enter billings, the best answer they could find to do this. Billings is defined as revenue plus change in deferred revenue for a period. Conceptually, when a SaaS order with a one-year prepayment term is signed, 100% of it goes to deferred revenue and is burned down 1/12th every month after that. To make it simple, imagine a SaaS company sells nothing in a quarter: revenue will burn down by 1/4th of starting deferred revenue [7] and the change in deferred revenue will equal revenue – thus revenue plus change in deferred revenue equals zero. Now imagine the company took an order for $50K on the last day of the quarter. Revenue from that order will be $0, change in deferred will be +$50K, implying new sales of $50K [8].

Eureka! We can see inside the SaaS machine. But we can’t.

Limitations of Billings as a SaaS Metric

If you want to know what investors really care about when it comes to SaaS metrics, ask the VC and PE folks who get to see everything and don’t have to impute outside-in. They care about

- New ARR growth

- Subscription growth margin

- Churn rates

- CAC and LTV/CAC (or increasingly, CAC Payback Period)

Of those, public company investors only get a clear look at subscription gross margins and the customer acquisition cost (CAC) ratio. So, looking outside-in, you can figure out how efficiency a company runs its SaaS service and how efficiently it acquires customers [9].

But you typically can’t get a handle on churn, so you can’t calculate LTV/CAC or CAC Payback Period. Published cohort growth, however, can give you comfort around potential churn issues.

But you can’t get a precise handle on sales growth – and that’s a huge issue as sales growth is the number one driver of SaaS company valuation [10]. That’s where billings comes into play. Billings isn’t perfect because it shows what I call “total subscription bookings” (new ARR bookings plus renewal bookings) [11], so we can’t tell the difference between a good sales and weak renewals quarter and a bad sales and a good renewals quarter.

Moreover, billings has two other key weaknesses as a metric:

- Billings is dependent on prepaid contract duration

- Companies can defer processing orders (e.g., during crunch time at quarter’s end, particularly if they are already at plan) thus making them invisible even from a billings perspective [12]

Let’s examine how billings depends on contract duration. Imagine it’s the last day of new SaaS company’s first quarter. The customer offers to pay the company:

- 100 units for a prepaid one-year subscription

- 200 units for a prepaid two-year subscription

- 300 units for a prepaid three-year subscription

From an ARR perspective, each of the three possible structures represents 100 units of ARR [13]. However, from a deferred revenue perspective, they look like 100, 200, 300 units, respectively. Worse yet, looking solely at deferred revenue at the end of the quarter, you can’t know if 300 units represents three 100-unit one-year prepay customers or a single 100-unit ARR customer who’s done a three-year prepay.

In fact, when I was at Salesforce we had the opposite thing happen. Small and medium businesses were having a tough time in 2012 and many customers who’d historically renewed on one-year payment cycles started asking for bi-annual payments. Lacking enough controls around a rarely-used payment option, a small wave of customers asked for and got these terms. They were happy customers. They were renewing their contracts, but from a deferred revenue perspective, suddenly someone who looked like 100 units of deferred revenue for an end-of-quarter renewal suddenly looked 50. When Wall St. saw the resultant less-than-expected deferred revenue (and ergo less-than-expected billings), they assumed it meant slower new sales. In fact, it meant easier payment terms on renewals – a misread on the business situation made possible by the limitations of the metric.

This issue only gets more complex when a company is enabling some varying mix of one through five year deals combined with partial up-front payments (e.g., a five-year contract with years 1-3 paid up front, but years 4 and 5 paid annually). This starts to make it really hard to know what’s in deferred revenue and to try and use billings as a metric.

Let’s close with an excerpt from the Zuora S-1 on billings that echoes many of the points I’ve made above.

Notes

[1] Source: William Blair, Inc., Zendesk Strong Start to 2018 by Bhavan Suri.

[2] Even though it’s not labelled as a driver and will break the renewals calculations, implicitly assuming all of it renews one year later (and is not spread over quarters in anyway).

[3] I’m not a financial analyst so I’m not the best person to declare which metrics are most typically released by public companies, so my data is somewhat anecdotal. Since I do try to read interesting S-1s as they go by, I’m probably biased towards companies that have recently filed to go public.

[4] As distinct from services revenues.

[5] Sometimes, however, those rates are survivor biased.

[6] And it worked to the extent that from a valuation perspective, a dollar of SaaS revenue is equivalent to $2 to $4 of on-premises revenue. Because it’s less volatile, SaaS revenue is more valuable than on-premises revenue.

[7] Provided no customers expire before the last day of the quarter

[8] Now imagine that order happens on some day other than the last day of the quarter. Some piece, X, will be taken as revenue during the quarter and 50 – X will show up in deferred revenue. So revenue plus change in deferred revenue = it’s baseline + X + 50 – X = baseline + 50.

[9] Though not with the same clarity VCs can see it — VCs can see composition of new ARR (upsell vs. new business) and sales customers (new customer acquisition vs. customer success) and thus can create more precise metrics. For example, a company that has a solid overall CAC ratio may be revealed to have expensive new business acquisition costs offset by high, low-cost upsell.

[10] You can see subscription revenue growth, but that is smoothed/damped, and we want a faster way to get the equivalent of New ARR growth – what has sales done for us lately?

[11] It is useful from a cash forecasting perspective because all those subscription billings should be collectible within 30-60 days.

[12] Moving the deferred revenue impact of one or more orders from Q(n) to Q(n+1) in what we might have called “backlogging” back in the day. While revenue is unaffected in the SaaS case, the DR picture looks different as a backlogged order won’t appear in DR until the end of Q(n+1) and then at 75, not 100, units.

[13] Normally, in real life, they would ask a small discount in return for the prepay, e.g., offer 190 for two years or 270 for three years. I’ll ignore that for now to keep it simple.

{kind=link}